BHP's economic and commodity outlook (FY20 full year)

18 August 2020

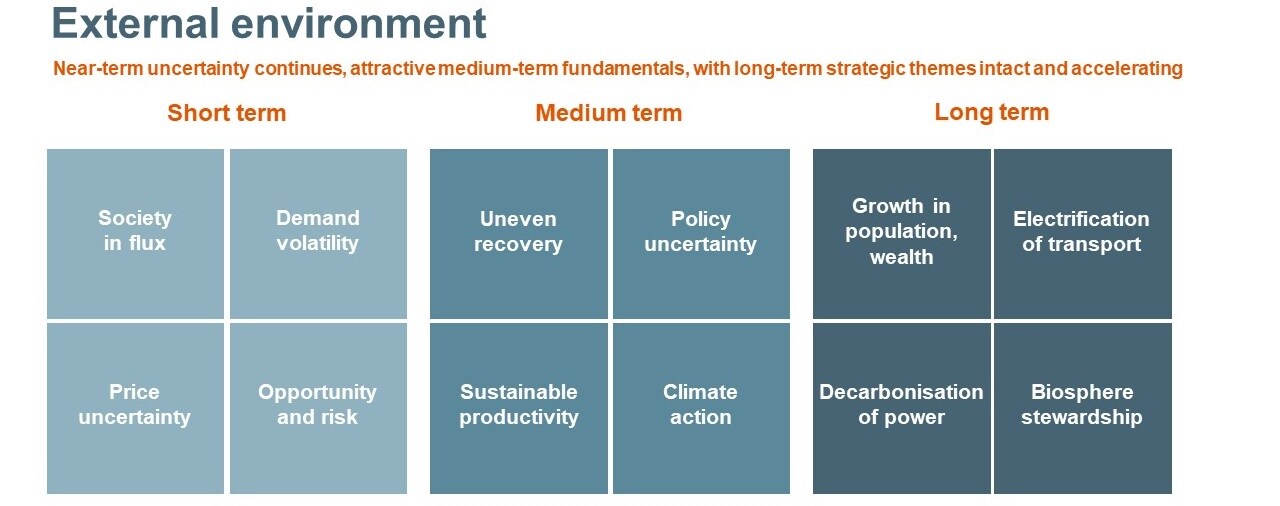

Six months ago, at the time of our half year results for the 2020 financial year, we had little conception of the size of the shock that was about to shiver the foundations of the world economy.

The result has been an extremely challenging demand, supply and price environment for many of our key commodities.1

For the 12 months ahead, we assess that weighted directional risks to prices across our diversified portfolio are mixed, albeit with the worst of the physical demand shock from COVID–19 hopefully behind us. How the likely re–emergence of COVID–19 outbreaks are managed by major societies is the main source of uncertainty in the outlook.

Within that portfolio wide judgement, we expect iron ore prices to ease from the spot levels observed at the time of writing, with considerable two–way volatility in prospect. Metallurgical coal still has to navigate a difficult period as major importing regions manage their re–openings in the first half of financial year 2021. COVID–19 permitting, sustained improvement is possible in the second half of the financial year.

Oil and copper prices are both highly susceptible to swings in global policy and economic uncertainty. Aside from this common trait, the fundamentals of the two commodities under COVID–19 have been very distinct.

Oil has suffered through a calamitous demand collapse, with the downdraft in pricing that this created only forestalled by a combination of very large withdrawals of supply and the partial normalisation of terrestrial mobility conditions. Copper demand has been much more resilient, reflecting the nature of its end–uses and its greater exposure to China’s recovery. Coupled with profound COVID–19 related difficulties on the supply side of the industry, this has enabled copper prices to recover quickly from the trough they initially fell into amidst the financial panic of March.

The over–riding caveat for all of our commentary is that while we hope that the COVID–19 outbreak is speedily contained everywhere that the first wave is still extant, and that elsewhere all subsequent waves are managed without a major impact on societal well–being, it would be unwise to be adamant about these matters. While we are all forced to live with these unknowns, there will be an uncertainty discount in the risk appetite of households and businesses. The impact this will have on real world decision making will constrain the global economy from running on all cylinders.

Looking beyond the immediate picture to the medium–term, we continue to see the need for additional supply, both new and replacement, to be induced across most of the sectors in which we operate: notwithstanding the reality that COVID–19 has significantly lowered the starting point for demand across most of our exposures.

In many cases, this could require higher–cost supply to enter the cost curve.

In isolation, the demand shock associated with COVID–19, some aspects of which can be reasonably expected to endure beyond the immediate horizon, is likely to delay the rational timing of such entries by a number of years versus pre–COVID estimates. This timing must then be adjusted based on the expected duration and scale of the direct and indirect impacts of COVID–19 on the supply landscape in each industry.

The combined impact of these factors could well delay the onset of inducement pricing in some industries but at this very early stage we do not feel that inducement prices themselves are in need of substantial revision.

COVID–19 has altered many things but it does not alter geology or define the frontier of operational efficiency in each commodity sector. Besides demand, these are the two most critical factors for identifying marginal sources of long run supply.

The projected steepening of some industry cost curves that we project, albeit delayed from prior expectations, can reasonably be expected to reward disciplined owner–operators with higher quality assets.

In the medium and long term, on the demand side, we continue to see emerging Asia as an opportunity rich region. China, India, ASEAN and the multi–decadal impact of China’s Belt and Road initiative are all expected to provide additional demand for our products.

As the true costs of a partial retreat from economic openness and a lack of climate action are progressively recognised, we anticipate a popular mandate for a more open international trading environment will eventually re–emerge, along with a concerted effort to confront climate change as a basic imperative.

We note that the younger generations that will define our future – both Millennials and Generation Z – are not only more concerned about a lack of action on climate change than their elders in both East and West, they are also more favourably disposed towards globalisation.2

On that uplifting note, we confidently state that the basic elements of our positive long–term view remain in place.

Population growth and rising living standards are likely to drive demand for energy, metals and fertilisers for decades to come.

We firmly believe that our industry needs to grow in order to build a better, Paris–aligned world.3

New centres of traditional demand will emerge where the twin levers of industrialisation and urbanisation are still developing today. Investment that seeks to adapt to, insure against and mitigate the impacts of climate change may eventually rise to become a material element of demand for parts of our portfolio. The electrification of transport and the decarbonisation of stationary power are expected to progress rapidly, as will the desire to tackle harder–to–abate emissions elsewhere in the energy, industrial and land–use systems. Comprehensive stewardship of the biosphere and ethical end–to–end supply chains will become even more important for earning and retaining community and investor trust.

The ability to provide and demonstrate social value to our operational and customer communities is both a core enabler of our strategy and a source of competitive advantage.

Against that backdrop, we are confident we have the right assets in the right commodities in the right jurisdictions, with attractive optionality, with demand diversified by end–use sector and geography, allied to the right social value proposition.

Even so, we remain alert to opportunities to expand our suite of options in attractive commodities that will perform well in the world we face today, and will remain resilient to, or prosper in, the uncertain world we will face tomorrow.

Table of contents

“The Great Lockdown”, as the International Monetary Fund has aptly dubbed the current global recession, has disrupted billions of people around the world and COVID–19 continues to ravage many developing nations that are ill–equipped to cope with such a pronounced call on their hard and soft infrastructure.

The developed world, and China, have fared somewhat better in combating the first wave of the outbreak, albeit with large national variation. The presence of mature existing health infrastructure allied to the ability to quickly mobilise productive and financial resources to both fight the virus and ameliorate the economic impacts of lockdown have put the developed world in a privileged relative position. At the same time, capital has flowed out of the emerging world, adding balance of payments and debt stress to the already crushing burden of COVID–19. As a result, we expect that 2020 is likely to see the first collective contraction in the economies of the developing world for more than 60 years.

Against this backdrop of unease, the US dollar strengthened on a real, trade–weighted basis over the 2020 financial year. However, the US dollar trend has reversed towards weakness in the early part of the new financial year.

The volume of global trade growth has collapsed under the Great Lockdown, falling by –17.7 per cent YoY in May. As global policymakers tentatively shift attention from cushioning the impact of COVID-19 to actively spurring recovery, it is worth recalling that the underwhelming performance of the global economy in calendar year 2019 was in large part due to weak international trade and the associated negative impacts on business confidence. Trade is an essential lubricant of global economic growth.

We strongly encourage policymakers to prioritise structural reforms at home as the surest route to sustainable productivity growth, and ultimately, prosperity, coming out of COVID–19. Remaining open to the cross border flow of people, goods, capital and ideas is vital to this end: free trade based on comparative advantage, competition, productivity and innovation are close companions.

These arguments highlight the importance of continued and vocal advocacy for free trade, open markets and high quality national and multilateral institutional design by corporations, governments and civil society.

The International Monetary Fund (IMF) expects the world economy to shrink by –4.9 per cent in calendar 2020 and grow by +5.4 per cent in calendar 2021. Within our range, our base case is similar measured across the two years. The associated quarterly path implies that under this case activity would return to the pre–COVID–19 level in the September quarter of 2021. More pertinent perhaps for thinking about the scale of the shock to commodity demand, our base case projects the world economy to be –6 per cent smaller than it would otherwise have been in calendar 2021 than if COVID–19 had not occurred.

The impact on the labour market has been profound. The International Labour Organisation (ILO) estimates that global hours–worked declined by –5.4 per cent in the March quarter and by –14 per cent in the June quarter of calendar 2020 (both measured against a December quarter of 2019 baseline). The June quarter figure is the equivalent to the loss of 400 million full–time jobs.4 The ILO predicts that the loss of hours will narrow to around –5 per cent by the December quarter of 2020, with their optimistic and pessimistic scenarios pegged in a very wide range of –1.2 per cent and –11.9 per cent respectively.

We note that by early July, policy support from the G–20 nations had reached $7.6 trillion, or 11.2 per cent of 2019 G–20 GDP. However, the gap between the surge in spending in the large developed economies in the G–20 (who have committed 13.8 per cent of their combined GDP) and the more modest response by the large developing countries (4.7 per cent of their GDP) is stark.5 The ILO estimates that at least 1.6 billion informal workers have had their livelihoods disrupted by COVID–19: and these people mostly live in the developing world, where the capacity to provide a safety net, temporarily or otherwise, is weakest. This has obvious implications for the rate at which developing economies will ultimately rebound from this crisis.

We argued in our March and June operational reviews that where “hibernation policies” have been enacted, a smoother resumption of activity than would otherwise have been the case might be reasonably expected. On the very limited evidence available to date, that has proven to be true so far. Further, indications are that liquidity support measures have been effective in dampening financial volatility. What is still highly uncertain is whether traditional monetary and fiscal stimulus policies will have below–average or above–average multiplier effects. A lower multiplier could result from depressed consumer and business confidence due to the deleterious impact of COVID–19 on both jobs and profitability. A higher multiplier could occur if the lagged impact of stimulus coincides with the release of pent–up demand as economies wake from hibernation. Overlaid with pessimistic and optimistic paths for COVID–19 containment respectively, each is a plausible book–end for assessing where the global economy might be at the end of calendar year 2021.

The arc of recovery will naturally vary widely across countries. We consider the major regions in turn below.

Back to top ↑

China

China’s economy shrank by –10 per cent in the March quarter, with almost two “lost” months (all of February and a few weeks either side) as hundreds of millions of workers were unable to return to their place of employment following the Lunar New Year festival. It is now, however, on a clear recovery track. Building sites and factories began to restart quite quickly over the course of March, albeit with considerable variability by location, size and ownership of firm, and industry. Large sequential improvements in construction and heavy industrial activity were observed in April, May and June, while services activity, consumer oriented manufacturing and personal mobility have been following with a slight lag, and on a flatter gradient. The economy rebounded +11.5 per cent in the June quarter, lifting YoY real GDP growth from –6.8 per cent in Q1 to +3.2 per cent in Q2.

The major risk to China’s V–shaped rebound is the possibility of a new wave of infections emerging (potentially from imported cases) that requires lockdowns to be reinstated on a macro–economically significant scale.6 That is among the range of pathways we consider and it is the key caveat for each of our regional outlooks. Domestic industrial activity though is not expected to flag this year or next for wont of policy support, as the state of credit growth, the stance of fiscal policy and the range of announcements (and re–announcements for signalling purposes) at the delayed “Two Sessions” collectively make clear. Negative feedback loops to China from the steep downturn in the rest of the world are factored in to our range analysis.

The above developments give China “first–in, first out” status on the initial wave of COVID–19, a point of difference that has left an indelible mark on global commodity markets in the year–to–date. At the time of our February results, when COVID–19 was still contained to China and its near neighbours, this is how we framed the uncertainty:

“The range of responses by the Chinese authorities to contain COVID–19, in tandem with the understandably risk–averse response of the population, will undoubtedly cause a sharp decline in economic activity in the March quarter. However, if the psychological and logistical impacts can be effectively contained within that window, construction and manufacturing activity (i.e. our steel and copper end–use sectors) should recover briskly to higher than normal run–rates in the June quarter.”

As we will recount in the commodity-specific sections, we have indeed witnessed some spectacular steel run–rates in the June quarter as the system sprinted towards annual goals. While an official GDP growth target was not announced for this year, such targets have always been an intermediate objective, a stepping stone for what really matters: the maintenance of full employment and the alleviation of poverty. While these goals are now being pursued with sustainable trade–offs on the environment and financial risks explicitly recognised,7 jobs have clearly emerged as first among equals in terms of leadership priority under both the Trade War of 2019 and the Great Lockdown of 2020.

Much of what we wrote six months ago on the expected performance of key end–use sectors feels redundant today.

Something that is common to our pre and post COVID–19 analyses is that infrastructure was bound to have a better year in calendar 2020 than in 2019.

In the second half of calendar 2019, the authorities expressed impatience that infrastructure was slower to respond to policy support than in previous fiscal easing cycles. Investment in transport projects was decent, but non–power utilities (e.g. waste treatment and water conservation) was a major under–performer relative to expectations, while grid spending did not meet budget. With trade hostilities with the US still running hot at the time, this was an urgent issue, and steps were taken to bolster the project pipeline and ensure financing was available to local governments. Unsurprisingly, infrastructure investment has been driving the recovery this calendar year in terms of both direct activity and its impact on upstream heavy industry. Importantly, confidence in the arrival of the infrastructure upswing made it possible for upstream sectors to restart with conviction in late February, early March, knowing that they would initially be burning a lot of working capital on finished goods inventory.

The recent floods have highlighted the importance of increasing investment in water related infrastructure and we anticipate further spending on this segment may yet be announced.

We anticipate that national level housing policies and rhetoric will remain directed towards limiting speculation, building rental markets and fine–tuning the shantytown redevelopment program. However, many local authorities have already proceeded to loosen controls where they can, with more than 60 cities and regions having eased either supply or demand side policies to support local property markets by the end of the March quarter. That has enabled a relatively swift rebound in sales volumes coming out of lockdown, with the level of activity back in the normal range in the June quarter.

Across calendar year 2020, housing starts are expected to decline mildly, mostly reflecting the steep declines during the lockdown. On a forward looking basis, some improvement is likely on a sequential basis in coming quarters. The long awaited rebound in housing completions is expected to firm and flow into calendar 2021, with around 10 percentage points of growth anticipated across the two years. Back on the policy front, an “urban residential communities’ renovation” program was announced at the Two Sessions, which aims to modernise facilities across 39,000 such clusters.

This should not be confused in scale with the shantytown program, but it will certainly be helpful, at the margin, for both manufacturing and construction jobs.

Auto production has inevitably lagged behind other areas of manufacturing, given the importance of Hubei province to the aggregate supply chain.8 However, auto sales have rebounded as lockdowns eased, and local governments in some major cities have provided direct support. Machinery production was expected to be very weak, but it has instead produced a positive surprise. Segments linked to infrastructure and domestic demand more broadly have been solid. Those more closely linked to international markets have been predictably weak. Consumer durables outside of personal computing are also constrained by weak export demand and have also been dealing with disrupted domestic retailing conditions.

On exports more generally, Chinese manufacturing benefited from the health equipment and consumables imperative and the work–from–home IT hardware boom but suffered from the steep decline in global discretionary household consumption and non-IT capital equipment. The aggregate outcome has been a more resilient picture than might reasonably have been expected, with exports of goods growing by 0.5 per cent YoY in the month of June, after a shallow contraction across the preceding four months. That compares to the –17.7 per cent decline in overall world trade described above.

Over the longer term, our view remains that China’s economic growth rate should moderate as the working age population falls and the capital stock matures.

China’s broad production structure is expected to continue to rebalance from industry to services and expenditure drivers are likely to shift from investment and exports towards consumption.

Nevertheless, China is expected to remain the largest incremental contributor to global industrial value–added and fixed investment activity through the 2020s even as its growth rates mature.

Within industry, we expect a concerted move up the manufacturing value–chain. This will require further improvements in the domestic innovation complex. Notwithstanding the natural emphasis now being placed on “dual circulation”9, given the times we live in, we anticipate that the concerted move outwards of recent years is likely to continue, with an emphasis on South–South cooperation, regional trade agreements10, and the Belt–and–Road corridors. More broadly, we anticipate environmental concerns will become an even more important consideration in future policy design than they are today.

Major advanced economies

The US economy’s eleven year expansion came to an abrupt end in calendar 2020. COVID–19 lockdowns led to both a steep contraction in economic activity and the loss of more than 20 million jobs.

In response, fiscal support of around $3 trillion had been mobilised as of early July, major central bank liquidity and asset purchasing programs have been instituted to calm financial markets, and policy interest rates have been cut by 1.5 per cent to around zero.

As of the middle of July, all US states had begun to reopen, with widely varying levels of success in terms of new infection rates. At least 20 states still retained material restrictions, while most states have announced school closure through the end of the academic year. The re–opening has allowed the labour market to begin the protracted healing process that will be required.

Beyond the obvious risks associated with COVID-19, the forthcoming Presidential and Congressional elections are a major additional source of uncertainty.

In Europe and Developed Asia, disruptions to manufacturing value chains were particularly difficult for the region to absorb, over and above common lockdown imposts on the broader economy.

In Developed Asia, Japan had a relatively difficult time suppressing its initial outbreak and it struggled to cope with the collapse in auto demand at home and abroad while also dealing with the financial and psychological blow of delaying the Tokyo Olympic Games. South Korea was somewhat more resilient, containing its outbreak quite effectively while also benefitting from the observed improvement in the global electronics sector.

In Europe, a variety of national responses to both lockdown and reopening have been put in place. Stimulus plans were slower to come to fruition than in the US and are of smaller scale, but they are arguably more strategic and effectively targeted. An emphasis on “building back better” by sponsoring an accelerated energy transition has been the clear theme. The agreement to finance recovery spending via mutualised public debt (European Commission bond issuance) is an important landmark for the European project.

India

India’s economy stuttered in calendar 2019 and then it collapsed under the pressures of COVID–19. Even among the large pile of spectacular statistical debris left in the wake of the Great Lockdown, India stands out. Two data points summarise the immensity of what the nation has been through. The first is that in April, a country with more than 1.3 billion residents did not record a single new car sale.11 Not one. The second is that India’s service sector PMI survey fell to a reading of 5.4 in April, where 50 is the expansion–contraction threshold. 5 point 4. And while the formal economy has clearly suffered, the informal economy, which provides four out of five non–farm jobs, has arguably been in direr straits, particularly in urban areas.

Against this backdrop, the government’s efforts to directly support the economy have been modest. The majority of India’s announced stimulus comes from the monetary side of the aggregate public balance sheet, with a focus on credit supply and liquidity support. Complementing these moves with a more decisive expansion of direct fiscal outlays on investment and income support would be a positive step towards accelerating the recovery path, which at present looks unappealingly flat.12

Returning India to a healthy medium–term growth trajectory will require a reduction in policy uncertainty, an increase in social stability, a greater focus on unlocking the country’s rich human potential, and an increase in international competitiveness in both manufacturing and traded services. The emphasis on moving up the “ease of doing business” rankings, and the steps taken to increase India’s share of geographically mobile foreign manufacturing investment that has come through during COVID–19 are both sensible steps. The decision to be less engaged with the regional trade agreement landscape though presents a mixed message in terms of reform appetite, given the positive impact that freer trade and increased competition would have on productivity growth and innovation.13

Steel and pig iron

Global crude steel production had become extremely unbalanced from a geographic perspective prior to COVID–19. In calendar 2019, China had expanded by around 8¼ per cent and the rest of the world had contracted by around –1½ per cent. The gap has widened further under COVID–19, with China on track to increase production moderately in calendar 2020, while ex–China output is expected to decline by a double digit percentage.

In calendar year 2019, Chinese production rose to just shy of the one billion tonne mark at 996 Mt. The approximate 2 per cent growth we project for calendar year 2020 will see reported annual production move comfortably above that “mystical” nine zero level.

China’s blast furnace utilisation rate increased from around 80 per cent in February 2020 to well above 90 per cent in June. Along with a 50–60 percentage point swing in electric–arc furnace utilisation (from a low of 12 per cent to around 60–70 per cent), that has led to a stunning crude steel run–rate of 1,117 Mtpa in June 2020 (+4.5 per cent year–on–year). Year–to–date annualised production of 1,004 Mt to June is broadly consistent with our base case. Pig iron is expected to grow slightly faster than crude steel in calendar 2020, reflecting constrained scrap availability for Chinese EAF mills.

The steel/pig iron relativity is then expected to reverse in calendar 2021, as scrap availability normalises, possibly assisted by a shift in import policy.

Finished steel inventories built up quickly in the March quarter as blast furnace operations consciously produced in advance of demand, trusting that sales would pick up when the lockdown was lifted.

This faith proved to be well placed, as finished inventories at mills fell swiftly though the June quarter as the various segments of downstream activity improved in sequence. The market for long products rebalanced most quickly, with daily rebar transactions well above normal seasonal levels for much of the June 2020 quarter. However, better than expected outcomes for domestic machinery and auto production have narrowed (but not fully closed) the gap between long and flat product performance seen early in the year.

We note that slightly less than 10 per cent of Chinese apparent steel demand is exported in finished products. That is a lower degree of external exposure than, say, Japan (around 14 per cent) or Germany (around 19 per cent). An additional 5 per cent of Chinese production is exported directly. Reflecting China’s status as the “clearing market for everything” through the June quarter, China’s net exports have fallen sharply to just +13Mt in the calendar year to June, with imports (including semi–finished products) up more than 30 per cent YoY while exports have declined by around –13 per cent YoY. The month of June itself saw China’s first steel trade deficit since 2008.

The unique circumstances of COVID–19 have altered a number of fundamental relationships across our commodity suite. In Chinese steel, the relationship between capacity utilisation and profit margins has been impacted. Profit margins have been slim this year despite the sharp increase in utilisation, with higher input costs and the large inventory run–up described above (+30 per cent YoY for mills plus traders) are two key reasons for that disconnect.

With the rebasing of the official capacity utilisation estimates earlier this calendar year, our own estimate of China’s long run equilibrium crude steel capacity utilisation rate is under review.

Turning to the long term, we firmly believe that, by mid–century, China will almost double its accumulated stock of steel in use, which is currently 7 tonnes per capita, on its way to an urbanisation rate of around 80 per cent14 and living standards around two–thirds of those in the United States. China’s current stock is well below the current US level of around 14 tonnes per capita. Germany, South Korea and Japan, which all share important points of commonality with China in terms of development strategy, economic geography and demography, have even higher stocks than the US.

We estimate that this stock will create a flow of potential end–of–life scrap sufficient to enable a doubling of China’s current scrap–to–steel ratio of around 20 per cent by mid–century.15

The exact path to this end–state is uncertain. Among the range of possibilities we consider, our base case is that Chinese steel production has entered a plateau phase, with the literal peak to occur no later than the middle of this decade. Our low case16 for China, which underpins our global view on steel–making raw materials, assumes that the peak year is contemporaneous. The industry is then assumed to immediately embark upon a multi–decadal decline phase in the annual output of both steel and pig iron, highlighted by an even more aggressive long–run scrap–to–steel ratio increase than the doubling outlined above.

Steel production outside China collapsed under the pressures of the Great Lockdown, with a double digit percentage decline across calendar 2020 in prospect.

Across the June quarter, at some point of which all major ex–China economies were in lockdown, utilisation in this group fell to between 50 per cent and 60 per cent, versus the norm of around 75 per cent in recent years.

In the calendar year to June, India’s crude steel output fell by –24.2 per cent while pig iron output fell by –19.4 per cent YoY. In the same period, Japan, Europe and South Korea contracted by –17.4 per cent (pig iron –15.8 per cent), –16.4 percent (pig iron –18.2 per cent) and –9.5 per cent (pig iron –8.7 per cent) YoY respectively. Note that the exposure to indirect exports of these three regions (with Germany as a proxy for Europe) sits between 14 per cent and 19 per cent. The Developed Asian producers are also highly exposed to direct exports, at 31 per cent and 20 per cent of production for Japan and South Korea respectively, versus a trivial 1 per cent for Germany.

The stark dichotomy between China and the rest produces a weighted global crude steel run–rate for January–June 2020 of –6.0 per cent (–3.6 per cent pig iron).

Indicators of a partial recovery outside China began to come through in June and July. India has been leading the way in terms of restarting offline capacity (noting that many restarted facilities are still running well below normal rates). We have seen signs that South Korean producers may bring capacity back online a little earlier than previously expected, while Japanese producers appear to have turned marginally more positive on the remainder of the year. The restart of downstream activities has also flowed through to somewhat better sentiment amongst our European customers.

Despite this tentative improvement, the full year global outcome for calendar 2020 is expected to be similar to the year–to–date actual, at close to –6 per cent for crude steel, and between –3 per cent and –4 per cent for pig iron. Our preliminary thinking on calendar 2021 is for a percentage bounce of similar magnitude to the 2020 contraction in crude steel, with pig iron lagging somewhat as rising scrap availability and lower scrap cost restores some competitiveness to the EAF fleet.

Iron ore

Iron ore prices (62 per cent, CFR) ranged between $80/dmt and $107/dmt over the second half of financial year 2020, averaging around $91/dmt. Prices have been strong. China’s V–shaped recovery has led to consistently strong port outflow. Lower than expected exports from Brazil have outweighed record shipments from Australia and the redirection of cargoes from Europe and Japan into China. Seaborne lump premia were volatile in the same time period, trading in the range of $0.11–0.32/dmtu and averaging $0.23/dmtu in the half.

Chinese port stocks touched a multi–year low point of 106Mt in June, and they closed the financial year below 110Mt. That is substantially lower than the closing position of 127Mt in calendar year 2019.

We consider that there are two major forces that could generate major iron ore price volatility in the coming year. The first is uncertainty regarding the re–emergence and containment of COVID–19 outbreaks. The second is seaborne supply uncertainty.

Six months ago, we offered up a third sponsor of price volatility in addition to these carry–over points: higher than normal intra–year demand volatility. We argued that:

“… if COVID–19 is effectively and demonstrably contained within the March quarter, we expect that an accelerated run–rate in the construction and manufacturing sectors for the remainder of the year can make up for the loss of activity seen at the outset of the year. … The sprint required to meet the annual plans of public and private entities in China in nine months rather than twelve (to stylise) will amplify the normal seasonal swings in steel end–use, potentially creating a shift from ‘famine‘ to ’feast‘ for the iron ore market.”

From the demand perspective, we defined the “famine” as a drop in the crude steel run–rate towards the mid–to–low 800 Mtpa range under lockdowns, and the “feast” as a run–rate approaching the never before seen 1.1 Btpa area. The reality has been that the famine never truly arrived: but the feast certainly did. Chinese blast furnace utilisation fell by only –7 percentage points in February, from around 87 per cent to around 80 per cent, which was a healthy figure given the circumstances. Utilisation then rallied sharply to above 93 per cent in the month of June, supporting a crude steel run–rate of 1117 Mtpa.17 The year–to–date pace is running close to 1 Btpa. With the economy–wide recovery on a relatively firm footing, we envisage an easing off from these explosive run–rates, not an abrupt step down, in the first half of financial year 2021. Therefore, “intra–year demand volatility” no longer earns a place as a top tier potential source of price volatility on a short term forward looking basis.

The observation that seaborne supply conditions for this calendar year and next are highly uncertain, both in aggregate and in terms of quality profile, is self–evident, as it has been since the Brumadinho tailings dam tragedy in January 2019. With Brazil now also struggling with one of the world’s most severe outbreaks of COVID–19, the recovery trajectory for exports is even more uncertain. While we do not think that the current constraints on Brazilian exports are informative for long run equilibrium pricing, we reiterate that the normalisation process could be a multi–year event. The inevitable ups and downs of the path back to a more stable and predictable Brazilian export performance can be reasonably expected to generate volatility in both index and product pricing.

We estimate that price sensitive seaborne supply increased by around 40 Mt (62 per cent equivalent basis) in calendar 2019. That was a rational response to the transitory nature of the conditions as they were perceived at the time. However, COVID–19 and other local factors have made it difficult for some smaller export jurisdictions to retain their 2019 run rates in 2020 to date, despite the attractive price environment. Exports from South Africa, Peru and the Brazilian juniors are all running behind their respective 2019 levels. Partially offsetting that, Indian exports have increased, with fewer domestic outlets for those tonnes under lockdown. We now estimate that much of the tonnage uplift seen in calendar 2019 may not eventuate in calendar 2020.

Chinese domestic iron ore concentrate production started the year at a low ebb under COVID–19, with the run–rate dropping from 211 Mtpa in December 2019 to just 187 Mtpa in February 2020. It has since recovered to 222 Mtpa in the month of July, slightly above the previous levels reached under “surge” conditions induced by attractive prices. Going forward, we expect that, in addition to structural market based drivers, safety and environmental inspections are likely to have a material influence on the average level and seasonal volatility of Chinese domestic iron ore production.

Our coastal blast furnace customers in China have experienced modest margins so far in calendar 2020. Different to calendar 2019 though, when coastal blast furnaces were operating at a cost disadvantage to both inland blast furnaces with captive iron ore and scrap–based EAFs, now it is EAFs suffering a competitive disadvantage due to high scrap prices amidst constrained availability, despite high seaborne iron ore prices. A wide gap between premium domestic coking coals and the seaborne equivalent is common across the two periods. China’s overall international competitiveness has also waned, with a steep increase in steel imports (included semi–finished products) pushing the net trade position into deficit in June 2020 for the first time since 2008 (as discussed in the steel and pig iron section). So while the underlying circumstances leading to narrower margins are somewhat different to calendar 2019, quality differentials have been relatively similar across the two years.

On the topic of differentials, we note that direct–charge materials – pellet and lump – saw their premia compress very late in the financial year 2020 and in the time since. This has partly been the result of pellet cargoes being directed from Europe into Asia: and Europe is a major consumer of direct–charge materials under ordinary circumstances. Specifically for lump, looser environmental enforcement this year (i.e. sintering restrictions), a strong Australian supply performance and the typical rainy season lull in demand have all contributed to rising lump port stocks, even as the level of fines inventory has ground consistently lower.

In the medium to long–term, the on–going Supply Side Reform and capacity swap, the expected migration of steel capacity to the coastal regions, the inexorable trend towards larger furnaces and more stringent environmental policies – Chinese controls being now, holistically, the most demanding in the world – are all expected to underpin the demand for high quality seaborne iron ore fines and direct charge materials such as lump. The South Flank project, which was approved in June 2018 and was 76 per cent complete at the time of writing, will raise the quality of our overall portfolio, in addition to increasing the share of lump in our total output.

Our opinion remains that around two–thirds of the movement in product quality differentials since the introduction of Supply Side Reform will be durable. The recent narrowing of differentials is an anticipated development on the path to this gravity point.18

We contend that the long run price will likely be set by a higher–cost, lower value–in–use asset in either Australia or Brazil. That assessment is robust to the prospective entry of new supply from West Africa, the likelihood of which has increased. This implies that it will be even more important to create competitive advantage and to grow value through driving exceptional operational performance.

Metallurgical coal

Metallurgical coal prices19 have ranged from a low of $106/t FOB Australia on the PLV index to a high of around $164/t during the second half of the financial year. MV64 has ranged from $89/t to around $148/t; PCI has ranged from $67/t to $103/t; and SSCC has ranged from $58/t to $85/t. Three–fifths of our tonnes reference the PLV index, approximately.

For the half year overall, the PLV index averaged $137/t, down by –9 per cent compared to the previous half and –33 per cent from the second half of financial year 2019. The differential between the PLV and MV64 indexes averaged 15 per cent in the second half of financial year 2020, 4 percentage points higher than in the previous half. Spreads within the non–PLV pool, on the other hand, have narrowed.

Metallurgical coal prices were under downward pressure for most of financial year 2020. In the first half of financial year 2020, broad based demand weakness in all major import regions but China was a weight on the price. Uncertainty regarding China’s approach to the volume of coal imports, both in aggregate and on a port–by–port basis, was an additional headwind for physical trade at times. In the second half of the financial year, COVID-19 demand impacts took over.

To understand the way metallurgical coal has traded over the last twelve months, it is important to be familiar with the demand profile. In the last “normal year” for the commodity, calendar 2018, seaborne imports of approximately 300Mt were shared relatively equally across China, Europe, India and Japan, with each region importing roughly between 50 and 60Mt. South Korea took an additional 33Mt (11 per cent), taking the share of the top five importers to around 86 per cent. China’s individual share was 18 per cent, with the other four taking 68 per cent. Compare that to the seaborne iron ore trade, where China accounts for close to three–quarters of the total.

Then recall that pig iron production in Europe and Japan fell outright in the second half of calendar 2019 as the global auto recession extended. Indian pig iron production growth also fell well below trend, reflecting the stuttering domestic demand environment. Furthermore, seaborne supply increased, mostly in the PMV bracket and Chinese import controls were an overarching concern. These factors combined to push metallurgical coal prices down quite rapidly from above $200/t in the first half of calendar 2019 to an average of $151/t in the second half, with a low daily spot price around $132/t.

That was the jumping off point for the industry as COVID–19 struck. Initially, prices rose on supply concerns, particularly in China itself and from neighbouring Mongolia. However, once it became clear that each of the major importers besides China would be going into lockdown, the logical conclusion was that the trade would have to clear almost exclusively through China for months, or even quarters, as the COVID–19 shock played itself out. That is essentially where the market still is today, notwithstanding the tentative green shoots of re-opening documented in the steel and pig iron section above.

As financial year 2020 closed, PLV prices had settled into a range between $105/t and $125/t that encompassed the 90th percentile of the C1 operating cost curve. Safety concerns at some mines in Queensland have helped sentiment to stabilise at these levels. Production impacts from these safety incidents have contributed to a –5.5 per cent YoY decline in Australian exports in the calendar year–to–May. Also, swing exports from the US are down materially (–20.5 per cent YoY calendar year–to–May); truck flow over the Mongolian border is roughly half normal levels, with exports down –52 per cent YoY calendar year–to–June; supply from Mozambique is also down; while Russia’s combined seaborne and landborne exports have fallen –19.1 per cent.20

Domestic Chinese hard coking coal supply has declined by –3 per cent year–to–date after a slow start due to COVID–19. Supply in the premium low–sulphur bracket, however, has increased 6 per cent YoY (noting the volume is still small at 0.75Mt) against a background of relatively attractive domestic prices. With pig iron production growing strongly, China’s call on imports should logically increase, notwithstanding the regulatory ambition to maintain a relatively flat level of total coal inflows versus recent history. Total imports of coking coal were up by 6.4 per cent YoY year–to–date to 76.5Mt annualised as of May. Shipments from Australia to China were up 8.8 per cent YoY to around 46.5 Mt annualised. China’s role as the near exclusive clearing market is illustrated by the gap between its imports from Australia (+8.8 per cent YoY), and Australia’s total exports (–5.5 per cent YoY).

Longer term, we argue that the continued policy focus on environmental considerations and financial sustainability in Chinese coal mining should increase the competitiveness of high quality Australian coals into coastal China, at the margin. Further, while there is always the potential for intra–year import curbs during lower demand periods, our view is that in the future, as in the past, these curbs will tend to mostly affect energy coal and non-PLV grades of met coal with higher sulphur content.

Similar to our view on iron ore, our technical and market research, and customer liaison, indicate that the premia that higher quality coking coals have attracted since China’s supply side reform are predominantly structural.

In coming years, most committed and prospective new supply is expected to be mid quality or lower, while customer intelligence implies that some mature assets are drifting down the quality spectrum as they age. The relative supply equation underscores that a durable scarcity premium for true PLV coals is a reasonable starting point for considering medium terms trends in the industry. The advantages of premium coking coals with respect to emissions are an additional factor supporting this overarching industry theme.

The flip side of PLV–privilege is that the non–PLV pool could face fundamental headwinds for an extended period in the disrupted post COVID–19 world.

On the topic of technological disruption, our analysis suggests that blast furnace (BF) iron making, which depends on metallurgical coal, is unlikely to be displaced by emergent technologies this half century. The argument hinges partly on the sheer scale of the existing stock of long-lived BF capacity (70 per cent of global capacity today, average fleet age21 of just 10-12 years in China and around 18 years in India). It also highlights the lack of cost competitiveness, technological readiness (or both) that will inhibit a wide adoption of theoretically promising alternative iron and steel making routes, or high-cost abatement levels such as hydrogen iron making and carbon capture and storage, for a couple of decades at least. We do, however, acknowledge that (a) PCI could be partially displaced in the BF at some point by a lower carbon fuel, and (b) the well-established electric arc furnace (EAF) technology, charged with scrap and without any need for metallurgical coal, will be a stern competitor for the BF at scale to the extent that local scrap availability allows. In a decarbonising world, EAFs with reliable scrap supply running on renewable power will be very competitive.

Our base case has the BF-BOF22 share of global steel-making capacity drifting down from 70 per cent today to between 55 per cent and 60 per cent in 2050, with EAF mills gaining that share.

Copper

Copper prices ranged from $4618/t to $6038/t ($2.10/lb to $2.73/lb) over the second half of the 2020 financial year, averaging $5500/t ($2.50/lb).23 The average was around –6 per cent lower than in the prior half and –11 per cent versus the equivalent half of financial year 2019. Price trends have been heavily influenced by a series of about–turns in investor risk appetite.

Six months ago, we wrote the following, in advanced of the escalation of COVID–19 outside China:

“In the absence of COVID–19, we assess that the forward looking fundamentals for copper would support an approximate trading range of $6000/t to $6500/t, based on an average rate of disruption to primary supply (i.e. an outcome closer to the historical 5 per cent loss, higher than the last two years). As matters stand, a return to that fundamental range is expected to require demonstrable containment of COVID–19.”

Looking back on that choice of words, and noting that the price has now returned to the range stated, a lay observer might reasonably assume that COVID–19 has been “demonstrably contained” and primary supply was on track for an “average” year of disruption. Unfortunately, neither of those things is true. COVID–19 is at best tentatively contained in China and the developed world, and it is demonstrably not contained in large swathes of the developing world, South America included. Supply disruption risks are therefore far higher than in a normal year.

Key events and phases in copper’s volatile price journey in the second half of the 2020 financial year were:

- The Stage One trade deal between the US and China, concluded just days before China announced its own outbreak;

- The escalation of COVID–19 cases outside of China and a sharp sell–off in pro–growth assets;

- The massive application of policy stimulus and liquidity support that followed, which enabled pro–growth assets to stabilise, and then recover;

- The developed world getting their initial outbreaks under control, which gave pro–growth assets an additional fillip;

- The broad realisation that China was experiencing a V–shaped recovery; and

- South America becoming the epicentre of the global COVID–19 outbreak, with associated risks to Peruvian and Chilean copper supply, which provided a copper–specific spur for prices over and above general macro sentiment.

Copper demand trends in China (roughly half of refined demand) will be starkly different to the rest of the world.

While both copper semis and crude steel are expected to experience a double digit decline in ex–China demand, we anticipate that the weakness in copper will be less severe. Conversely, in China, copper demand is expected to be marginally weaker than steel in the 2020 calendar year, based partly on copper’s greater exposure to indirect exports (approximately 20 per cent versus approximately 10 per cent for steel). Copper also benefits less than steel from the upswing in transport and non–power utilities infrastructure, which are the focus of strong policy support. The sources of resilience in the Chinese copper demand picture are post COVID–19 upward revisions to the power infrastructure budget, the solid outlook for housing completions and the better than expected performance from the machinery sector, as detailed elsewhere in this report.

Our preliminary base case for calendar 2021 has global copper semis demand recovering to a level just short of the calendar 2019 total. Within that, Chinese demand is expected to be 3–4 per cent higher than it was in calendar 2019, with ex–China demand a similar amount lower than the equivalent benchmark. Reflecting both macro and viral uncertainty, the low–high range around that base case is wide.

On the supply side of the industry, Chile and Peru, the two largest exporters of primary copper, have both experienced difficulty in containing COVID–19, with flow–on impacts to copper operations and the broader supply chain. This has led to a material tightening of the copper concentrate balance, with treatment and refining charges moving lower in response, despite challenged smelter profitability. Scrap availability has also been constrained globally, for both logistical and economic reasons. As of July 31, Wood Mackenzie had identified 890kt of disrupted production year–to–date, equivalent to 4 per cent of their initial annual production expectations. That is well ahead of the disruption pace seen in the prior year, and it is reasonable to expect it to rise further as new information officially comes to hand. At the same point of calendar 2019, the rate was 2.2 per cent, while the full year outcome for 2019 was 4.8 per cent. The South American mining industry at large is facing understandable issues with employee absenteeism as COVID–19 risks heighten, especially in localities where hospital capacity is under pressure. The continent provided 42 per cent of the world’s primary copper in calendar 2019.

Turning to the medium term outlook, the net effect of the COVID–19 shock is tentatively expected to push back the timing of inducement pricing by one or two years versus prior estimates, principally due to the lower starting point for demand. While demand could be more volatile than supply in the early years of adjustment, committed supply (including our Spence Growth Option, which is 93 per cent complete at the time of writing and is expected to be commissioned between December 2020 and March 2021) and rising scrap availability should keep the market close to balance. Beyond that near–term window, depending upon exact project timing and year–to–year demand swings, the expected arrival of a cluster of new supply from Peru, Chile, central Africa and Mongolia in the calendar 2021 to 2024 period could temporarily tilt the market into modest surplus in one or more of those years.

Subject to the above caveats on precise timing, a structural deficit is expected to open in the mid–to–late 2020s, at which point we see some sustained upside for prices.

Long term demand from traditional end-uses will be solid, while broad exposure to the electrification mega-trend offers attractive upside.

Grade decline, resource depletion, increased input costs, water constraints and a scarcity of high–quality future development opportunities are likely to result in the higher prices needed to attract sufficient investment to balance the market.

It is these parameters that are critical for assessing where the marginal tonne of primary copper will come from in the long run and what it will cost. We estimate that grade decline could remove –2 Mt per annum of mine supply by 2030, with resource depletion potentially removing an additional –1½ and –2¼ Mt per annum by this date, depending upon the specifics of the case under consideration.

Our view is that the price setting marginal tonne a decade hence will come from either a lower grade brownfield expansion in a lower risk jurisdiction, or a higher grade greenfield in a higher risk jurisdiction. Neither source of metal is likely to come cheaply.

Crude oil

Crude oil prices (Brent) ranged from a low of around $17/bbl to a high of around $69/bbl in the second half of financial year 2020. Brent was down by around –34 per cent from the average of the prior half. West Texas Intermediate (WTI) ranged from –$37/bbl to $63/bbl, with the front–month trading below zero for the first time in history on April 20.

The front–month Brent minus WTI spread was materially narrower on average half–on–half, contracting to $3.98/bbl in the second half of the financial year 2020 from $5.57/bbl. The WTI minus MARS24 spread averaged around –$2/bbl in the first half of the 2020 financial year and –$0.93/bbl in the second (i.e. MARS at a premium to WTI) reflecting the ongoing impact of the (relatively) tighter market for sour crudes post the Venezuelan collapse and loss of Iranian barrels due to US sanctions. In calendar year 2017, in an “undistorted” operating environment, this spread was +$0.16/bbl.

While the long run economic, geopolitical and industry–specific consequences of COVID-19 are not yet known, we can say with certainty that no future history of the global energy system will be complete without a retelling of these dramatic events.

Two far left hand side tail risks came together in March 2020 to send the oil price tumbling to a three standard deviation collapse.25

The first was the breakdown of OPEC+ talks on March 6, which caught a complacent market completely by surprise. Rather than the collegial rubber stamping of the recommendation of the OPEC Joint Technical Committee that the markets were expecting, the Kingdom of Saudi Arabia (KSA) left the failed meeting determined to impose their will on the wider industry. By announcing a steep ramp up in production, while simultaneously offering their premium crudes at a discount in selected regional markets and chartering the bulk of available VLCCs (Very Large Crude Carriers) to transport the spike in anticipated product, the KSA openly declared a price and market share war.

The second was, of course, the Great Lockdown, which grounded flights, slashed traffic flows and sent oil products demand crashing at unfathomable speed. It is truly remarkable that the greatest episode of oil demand destruction in history occurred just as the KSA decided to launch its production and discounting offensive.

The impact on price was immediate and brutal. In North America, it quickly became apparent that with a previously unthinkable glut of supply to address, access to land storage would be the critical enabler for inland crudes (i.e. unable to evacuate/store by/at sea) to keep operating. Regional differentials to WTI Cushing widened sharply. Pipeline operators began asking for hard proof that a purchaser or storage facility was waiting at the other end of the journey. And then, on Monday 20 April, the front–month WTI Cushing contract itself, which was due to expire on the following day, collapsed below zero and kept falling to an intra–day low of –$40/bbl, before closing at –$37/bbl. While speculative dynamics in financial markets rather than physical fundamentals brought about this extreme outcome, the physical market for some stranded inland crudes had already traded below zero prior to this event. These events underscore both the degree of stress across the industry as a whole and the reality that in some very specific circumstances, oil above the ground temporarily became a liability rather than an asset.

With the benefit of hindsight, one can see that as the joint occurrence of a producer price war and a –20 to –30 Mbpd collapse in the demand run-rate was unthinkable, a previously unthinkable price was the appropriate denouement for this remarkable confluence of events.

Since that nadir, a combination of very large cuts to supply (with OPEC+ back at the negotiating table), China’s V–shaped recovery and selective reopening in other major economies have enabled the Brent price (which bottomed out just below $20/bbl) to retrace around half of its losses. Brent was trading in the low-to-mid $40s per barrel at the time of writing.

While we are comfortable that the most significant physical risks to the market have passed, the recovery path from here is highly uncertain. The re–escalation of COVID–19 cases in many US states, and the consequent likelihood of renewed restrictions on mobility, is one cause of concern for oil product demand. There is also an abundance of supply that can come out of storage, on land and at sea, to flatten the recovery profile for price even as demand picks up. These are likely to be the first barrels that come back in to circulation. After that, there is the tapering of OPEC+ cuts from –9.7 Mbpd to –7.7 Mbpd from August to contend with and the possibility of lower cost US shale assets hedging their way back in if the forward curve steepens just a little.

There are upside risks as well. Under ordinary circumstances, 1 percentage points of growth in world GDP tends to be associated with 0.3–0.5 percentage points of oil demand growth. However, oil demand has fallen by much more than GDP in the year to date due to the unique circumstances of the Great Lockdown. Roughly speaking, we estimate that the ratio was not 0.4 to 1 through the June quarter: it was more like –2.5 to –1. That is an 8 fold increase in sensitivity. On the way back up, it is a reasonable expectation that product demand will grow more rapidly than GDP, given the swift release of oil–dependent mobility that comes with the easing of lockdowns.

The arithmetic above is important for considering the relative steepness of the initial rebound. After that reset, the reality is that the world economy will be smaller than it would otherwise have been for some time to come, and the level of oil demand is also expected to be lower than it would otherwise have been.

Shifting to the longer term, while demand has been hit very hard in the short–term, it is still highly uncertain to what degree, if any, demand has been impaired structurally. Our preliminary analysis points to potential headwinds coming from the loss of vehicle miles travelled as a portion of commuter trips are lost due to working from home; reduced aviation intensity; policy support for EVs that could drive uptake closer to our current high case for in terms of fleet and sales26; and the possibility of cash–for–clunkers programs that retire older vehicles and thus increase the efficiency of the fleet. Weaker economic growth in the populous developing countries hardest hit by COVID–19, leading to slower uptake of auto ownership and slower growth in demand for logistics and air travel, is a further possibility.

Potential tailwinds could emerge from an increased preference for private cars over public transport in emerging Asia; an increased preference for car ownership over ride–hailing or sharing services; and an increased need for packaging and extra vehicle miles to accommodate the embedding of the online–to–offline consumption mega–trend. And most simply, lower oil prices increase affordability, which is not a trivial considerations in the developing world. Lower oil prices also delay the timing of EVs becoming cost competitive versus internal combustion engine (ICE) vehicles in the mass market segment (for a given battery learning curve assumption), potentially pushing against the policy support described above. On the other hand, low oil prices may also encourage governments to reform costly fiscal subsidy regimes, an opportunity most recently highlighted by the International Energy Agency (IEA).27

The supply side of the industry is adjusting rapidly too. Large and small firms alike have signaled considerable reductions in capex plans. According to consultancy Rystad, final investment decisions (FIDs) for greenfield projects have fallen back to 1950s levels. Wood Mackenzie projects that half a trillion dollars in upstream development and exploration spending could be lost out to 2025. The IEA is predicting a –33 per cent decline in upstream petroleum capex in calendar 2020 and a –31 per cent decline in downstream and infrastructure. The oil rig count in the US is down more than –70 per cent, back to pre–shale boom levels. Combined, the petroleum value chain is set for its smallest real capital outlay in the history of the IEA’s series, which goes back to 2010. In a sector subject to the perpetual tyranny of field decline, with (conservatively) a third of on–stream barrels needing to be replaced on a rolling ten–year cycle, that is also coming off a relatively unsuccessful decade for exploration, an investment and exploration crunch of this magnitude is expected to have major ramifications for supply for some time to come.

The discussion above highlights that the attractiveness of oil as a commodity cannot be seen solely through a demand lens. (For our pre–Covid views on oil attractiveness, please go here.) Treated in isolation, the short term demand loss that COVID–19 has brought about is very likely to push back the timing of when the industry will need to induce the new deepwater projects that we expect to provide the marginal barrel in the long run. However, our ranges also incorporate plausible cases where a capex ice age allows impaired supply to fully mitigate the demand shock in the medium term: and of course we range the demand shock itself.

Our base case is that demand will rise modestly above pre-COVID levels in the coming years, before reaching a plateau in the medium run. In the phase that precedes the plateau, the twin disruptive levers of efficiency and electrification that are operating on the road transport segment are more than offset by the impact of rising living standards in the developing world. But these circumstances will not last forever. Beyond the plateau, which we expect could be sustained for a considerable time, we foresee a steady erosion of demand as the disruptive forces gain ascendancy over the traditional economic development drivers, assisted by technological progress. The ability of developing countries to leapfrog in their technology choices as cost relativities evolve (subject to infrastructure availability) is expected to ensure that their future pathways of oil use per head track somewhat lower than the historical pathways pursued by the major OECD economies. Future patterns of urban infrastructure design and country specific population density and agglomeration characteristics also play a role in this assessment.28

Bringing this bottom-up analysis of demand together with the systematic decline rates of at least 3 per cent per annum that the supply side of the industry is subject to, points to an expected structural demand-supply gap through at least the mid-2030s. Considerable investment in conventional oil is going to be required to fill that gap. Our conservative views on both US onshore geology and the underlying shale productivity trend, which ultimately encouraged us to exit the shale business, are strongly held. We deem that deepwater assets are the most likely major supply segment to balance the market in the longer term. The price expectation required to trigger investment in new deepwater projects is believed to be significantly higher than the prices we face today.

Oil will be attractive, even under a plausible low case, for a considerable time to come.

Liquified natural gas (LNG)

The Japan–Korea Marker (JKM) price for LNG averaged $2.89/MMbtu DES Japan in the second half of 2020 financial year, –45 per cent lower than the prior half, with the price ranging from $1.83 to $5.35/MMbtu. Prices were weighed down by the steep decline in demand produced by the Great Lockdown, which combined with new supply coming on–line in a market that was already facing a supply glut prior to COVID–19. Sharply lower crude oil prices also had an impact at the margin. Europe again served as an outlet to absorb excess cargoes, leading to very high utilisation of storage for the time of year. Under these extreme conditions, the economics of US LNG exports collapsed, leading to more than 160 cargo cancellations in the year–to–date (up to September lifting).

Six months ago, the forward curve was pricing shoulder season JKM close to $3/MMBtu. While that was a depressing figure to see on the screen at the time, actual prices have been even weaker as the reality of North Asian and European lockdowns set in. It remains important to note that this is not necessarily where all producers and consumers will transact. The majority of LNG molecules still change hands under long term oil linked contracts, although the proportion has been declining in recent years. Even so, with Brent plunging below $20/bbl at one point, realised prices for oil–linked contracts also moved to historical lows.

On the supply side, a large increment of new production came to market in calendar year 2019, with the overflow from incomplete ramp–ups influencing fundamentals in 2020. However, that overflow has been less than previously expected, largely due to the aforementioned cargo cancellations in the US. Further, for the large pipeline of projects where first gas is anticipated in calendar 2020, actual production is expected to come in much further below nameplate than previously anticipated. That implies a substantial shadow effect on 2021, in our view, but these slower ramp–ups are, in aggregate, a sensible response to the deeply over–supplied market.

Looking further ahead, within our generally constructive outlook for LNG demand growth the key uncertainties are Chinese energy mix policies and the scale of competing supply of indigenous and pipeline gas; the level of investment in new gas infrastructure in India; the timing and scale of nuclear restarts in Japan and energy mix policies in South Korea. Outside Asia, the amount of Russian pipeline gas supplied to Europe also represents a swing factor for the outlook.

Despite the strong LNG demand growth that we project, current and committed capacity is likely to amply supply the market until the middle of this decade, with considerable overflow from Asia to Europe expected at times. Beyond the mid–2020s new projects are expected to be required in a global gas market where the marginal supply looks likely to come from North American LNG exports under a range of scenarios.

Five of the six new projects that produced first gas in calendar year 2019 were US export facilities; as are four of the six projects coming online in calendar 2020. With US supply able to swing between the two major consumer markets of Europe and Asia, thereby drawing them closer together, a greater US export presence is a supportive signpost for the hypothesis that regional gas hubs are on a path to harmonisation around a global benchmark.

In the longer term, we see LNG as a commodity that has an opportunity to operate under inducement economics, at times, given the combination of systematic base decline and an attractive demand trajectory. Global gas is also a big market that is getting bigger, with LNG expected to almost double its share of that expanding pie. However, gas resource is abundant and liquefaction infrastructure comes with large upfront costs and extended pay backs. The answer to this complicated equation is that only assets that are advantaged by proximity to existing infrastructure, or customers, or both, are attractive to us. For a more detailed discussion of LNG attractiveness, please go here.

Eastern Australian gas

The fundamentals of East Australian natural gas continue to evolve. The rise of Queensland LNG projects fed by coal-bed methane resources and the maturation of conventional fields in Bass Strait and the Cooper Basin have combined to irrevocably alter the fundamentals of domestic price formation. Our firm assessment is that the East Australian market will ultimately harmonise around LNG netback pricing. The likelihood of LNG imports being required as a seasonal source of incremental supply in the southern states has increased. We expect that this development would accelerate the harmonisation process, as would improving the transparency and depth of domestic price discovery mechanisms.

Prices lost ground over the second half of the 2020 financial year. The combination of lower demand under COVID–19, lower international spot LNG prices and more gas being made available to the domestic market all put downward pressure on prices in eastern Australia. An increasing connectivity to global gas dynamics was evident.

Looking beyond the temporary operating conditions seen over the last six months or so, whilst there is industry consensus that there is an ample indigenous resource base to meet long term domestic demand, the future cost to extract and process this resource appears to be rising. Further, constraints on onshore development hinder the efficiency with which the industry might otherwise operate. As traditional sources of supply fall off or plateau, new upstream investment will be required. To accommodate timely investment in competitive incremental supply, a clear and stable policy foundation is required.

We continue to believe that a more accommodative policy environment for onshore gas development – both conventional and unconventional – has the capacity to provide significant additional supply to the market at reasonable cost. Such an approach should help to encourage the new investment necessary to provide for reliable and affordable gas supply over the long term. It also has the clear benefit of allowing market forces to allocate capital where it will be most effective in achieving those ends.

Energy coal

Energy coal prices were weak in the second half of financial year 2020.

The gCNewc 6000 kcal/kg FOB Newcastle index (hereafter 6000kcal) averaged around $61/t over the half, down from around $68/t in the first half of financial 2020. Prices ranged from a high of around $74/t to a low of around $50/t. That is below the 2015/16 trough in real terms. Based on the Wood Mackenzie operating cost curve, more than half of seaborne supply (comprising all grades of energy coal) was likely experiencing negative margins with 6000kcal prices in the low $50s.

The 5500kcal index averaged around $49/t over the same period, with a high of around $58/t and a low of around $38/t, which was where it closed out the half year.

The spread between the spot indexes for gCNewc 6000kcal and 5500kcal reverted to historical average of close to 20 per cent in the second half of financial year 2020, down from around 30 per cent in the 2019 calendar year.

While not directly relevant to our business, there was a compression of spreads between the lower grades of energy coal (the 5000, 4200 and 3400 gross–as–received29 kcal brackets) as prices traded deep into the cost curve. Supply has been “sticky” in most export jurisdictions, with the exception of Indonesia, where output has been materially lower. Indonesian supply is prominent in these lower quality brackets. Developed Asian markets, who are the largest buyers of >5500kcal product, have been weak under the shadow of COVID–19. Japanese imports contracted by –3 per cent YoY in the first half of the 2020 calendar year, while power demand was down -4 per cent YoY, South Korean imports contracted by –11% per cent.

Chinese demand for seaborne energy coal rebounded as lockdowns were lifted, with consumption of coal at coastal power plants back in the normal seasonal range by April 2020. Hydro generation has been inconsistent, along with the weather, with dry conditions early in the year then giving way to floods. The market consensus has been that the 271–281 Mt import inflow registered in calendar years 2017 and 2018 would serve as an informal objective for total coal imports (including metallurgical and lignite) in calendar 2020, rather than assuming that the jump to around 300Mt in 2019 was the new norm. Enforcement of quotas by month and by port, including clamping down on the practice of trading firms clearing customs at one port but discharging at another, have been somewhat effective. Even so, with so much product being forced to clear to China under the Great Lockdown, some provinces and individual ports had already exhausted full year quotas by May.

India saw a sharp decline in energy coal imports in January – June 2020 (–27 per cent YoY). Power demand declined by –7 per cent YoY in the same period, while domestic coal output was quite resilient, at –3 per cent YoY.

Demand from the Atlantic and Mediterranean regions was weak in advance of COVID–19 and lockdowns have deepened the malaise. In calendar 2019, the weakness reflected commercially driven coal–to–gas switching in parts of Europe, where relatively cheap pipeline gas and LNG imports, plus a steep rise in the price of European Carbon Allowances (ECAs)30, have driven generator behaviour. In calendar 2020 to date, all of these factors have remained in place and in some instances they have been amplified by COVID–19: and demand for power itself has now fallen sharply. Renewables have been able to take a larger share of that shrinking pie.

Longer–term, we expect total primary energy derived from coal (power and non–power) to expand at a compound rate slower than that of global population growth.

Coal power is expected to progressively lose competitiveness to renewables on a new build basis in the developed world and in China. On a conservative estimate, the cross over point should have occurred in these major markets by the end of this decade. However, coal power is expected to retain competitiveness in India, (where the coal fleet is only around 10 years old on average: one quarter of a normal lifetime), and other populous, low income emerging markets, for a much longer time.

Back to top ↑

Potash

Muriate–of–potash (MOP) prices31, which were trending downwards for much of the 2020 financial year, now appear to have bottomed, with some signs of recovery in Brazil. Brazilian gMOP32 spot prices touched $210/t CFR in April, equalling the last cyclical low set in July 2016. However, they have since firmed, reaching $230–235/t in mid–July. The peak to trough move in Brazilian prices was –$145/t.

New contract settlements by China in April (down –$70 to $220/t CFR) and India in May (down –$50 to $230/t CFR) provided other regional markets a foundation to build upon. In June 2020, the FOB standard grade Vancouver benchmark midpoint was down by around –21 per cent YoY to $215/t. In the March quarter of 2020, Canada’s Nutrien reported an average realised price of $180 ex–mine.

This figure is –24 per cent lower YoY (–$58) but is still $30 higher than the lowest realised price of the last decade, which was reported in the September quarter of 2016.

Global shipments declined by –5 per cent YoY in calendar year 2019 to 64Mt. Headwinds for demand included a very wet spring in the United States, a late onset of the monsoon in India and weak palm oil prices hitting farm incomes in Southeast Asia. Having built up substantial inventories in the first eight months of calendar 2019, China was largely absent from the import market from September 2019 until the settlement of new contracts in late April 2020. COVID–19 impacts on downstream demand in some regions, particular those that have enforced strict lockdowns, such as China, India and Malaysia, have been enough to dampen expectations of a strong global rebound in calendar 2020.33

The last few years are a microcosm of the history of potash demand. While trend growth in demand is quite reliable over longer time periods, reflecting the stability of the basic drivers, one cannot rely on any particular year exhibiting trend–like growth, given the potential impact in any specific time period of weather, swings in farm incomes, exchange rates, changes in relative affordability vis–à–vis other fertilisers and altered subsidy policies, to name a few.