Pathways towards steelmaking decarbonisation

- We’re working to support industry to develop steel production technology capable of 30 per cent lower greenhouse gas (GHG) emissions intensity relative to conventional blast furnace steelmaking by 2030.

- We’re collaborating with eleven steelmakers – representing around 22 per cent of the world’s reported steel production – on a range of projects to support this goal.1

- To reduce emissions intensity at scale, we need to find pathways to reduce GHG emissions from conventional blast furnace steelmaking, which currently represents 70 per cent of global steel production.

- We are pursuing a portfolio of projects, and have co-invested in, Direct Reduced Iron pathways (including the Electric Smelting Furnace), innovative electrolysis-based technology, and blast furnace emissions reduction (including carbon capture).

- The total of current committed and planned funding from us and our estimate of committed or anticipated funding and in-kind contributions from our strategic partners from FY2020 to FY2029 in support of steelmaking GHG emissions intensity reductions is approximately US$420 million, based on available information and our assumptions as set out in our Climate Transition Action Plan 2024 (CTAP).2

In recent years, BHP has increased its exposure to commodities that we anticipate being in demand due to the trends that will shape the world for decades to come, including decarbonisation and electrification, urbanisation and a growing global population.

Copper for electrification of transport and energy networks. Potash to underpin our food security through more sustainable land use. And more iron ore and steelmaking coal for use in steelmaking, to develop our cities and build renewable energy and other infrastructure.

Greenhouse gas (GHG) emissions from steelmaking represent the majority of BHP’s reported Scope 3 emissions inventory. This presents an opportunity for BHP to work with our steelmaking customers to support them to develop steel production technology capable of producing less GHG through the value chain.

As detailed in our 2024 Climate Transition Action Plan, we have a medium-term goal to support industry to develop steel production technology capable of 30 per cent lower GHG emissions intensity relative to conventional blast furnace steelmaking by 2030. And we have a long-term goal of net zero Scope 3 GHG emissions by CY2050. Achievement of this goal is uncertain, particularly given the challenges of a net zero pathway for our customers in steelmaking, and we cannot ensure the outcome alone.

BHP’s steel decarbonisation framework

For the world to decarbonise and still produce the steel needed to meet the demands of increasing urbanisation, population growth and energy transition infrastructure, widespread deployment of near zero emissions3 steelmaking technology is going to be needed.

Near zero emissions steel can be produced from scrap metal today in an Electric Arc Furnace (EAF). However, production is limited by the availability of scrap and, as such, we expect ore-based steel production to continue to be a vital part of the steelmaking industry.

Today, integrated steelmaking via blast furnaces is the predominant steelmaking processing route, representing approximately 70% of global production. While this route has evolved to become more energy efficient over time, it remains GHG emissions intensive. But because of its widespread use and a young blast furnace fleet in steelmaking regions such as China or India, reducing emissions in the blast furnace processing route where available, must be a part of the roadmap towards decarbonisation.

It is with this in mind that we have developed our steel decarbonisation framework.

The pathways towards steelmaking decarbonisation

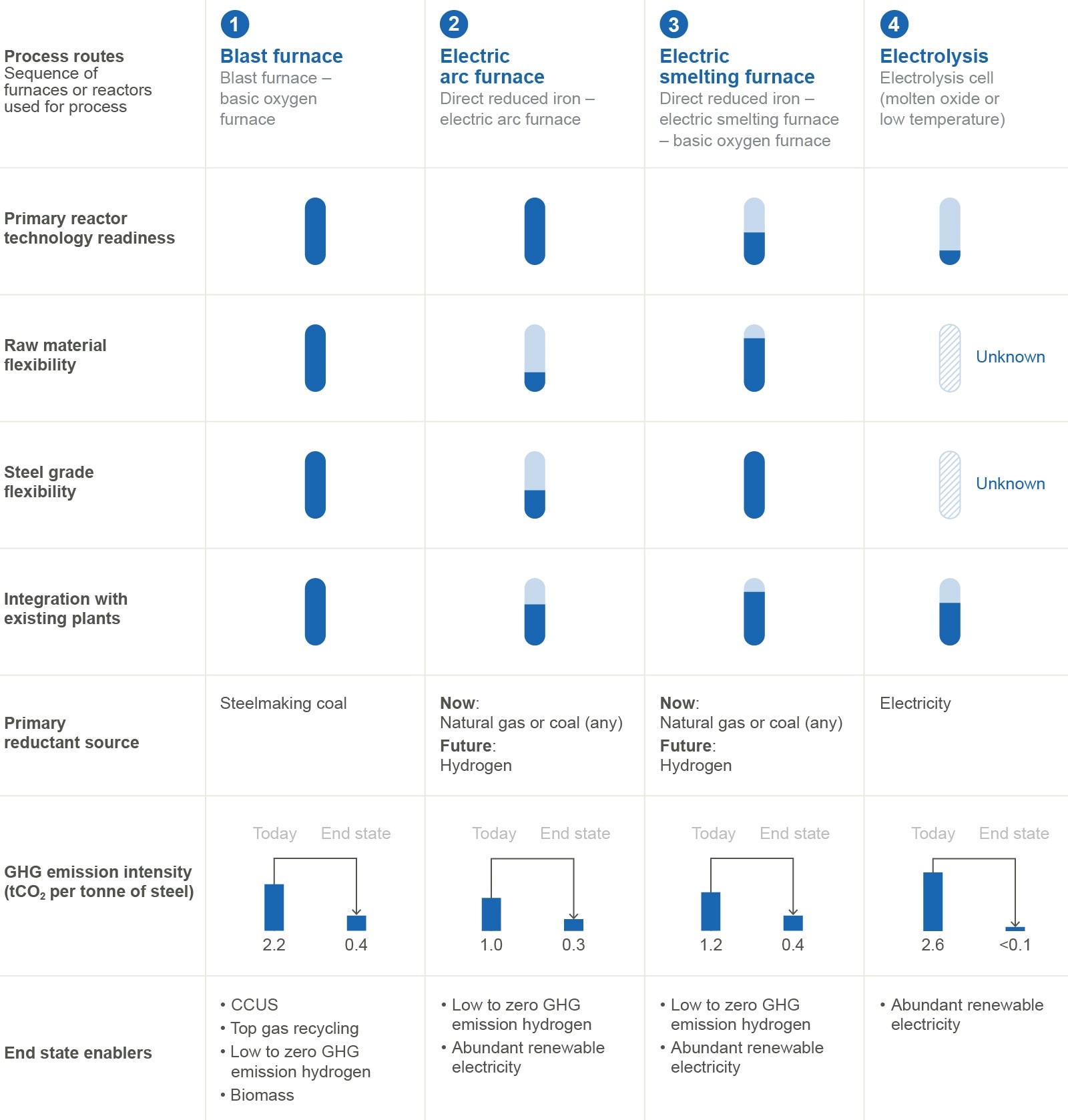

Four process routes, in our view and as represented in the pathways that our customers are investigating, offer potential for developing into a feasible pathway for producing near zero emissions steelmaking with sufficient flexibility, scalability and efficiency to support widespread adoption. The four process routes are:

- Blast furnace

- Direct reduced Iron (DRI) - Electric arc furnace (EAF)

- Direct reduced Iron (DRI) - Electric smelting furnace (ESF)

- Electrolysis

The blast furnace is the only one of the four pathways that relies on steelmaking coal as an input, while the other three pathways require significant volumes of low or zero GHG emissions electricity, and the gradual replacement of natural gas with hydrogen in the DRI process step.

Estimates of the typical GHG emissions intensity in the end state for decarbonisation in the four process routes are shown in the following diagram

Diagram 1: Estimates of typical greenhouse gas emissions intensity in the end state for the four technology pathways in BHP’s steel decarbonisation framework (Figure 2.3, page 22 of BHP’s 2024 Climate Transition Action Plan)

The pathways and stages of progression that individual steelmakers may take will vary.

A range of factors will influence the investigation and progression of these potential pathways, including government policy and regulatory settings, capital stock (including the age of existing infrastructure), the availability, grade and cost of iron ore and scrap metal, the availability of low to zero GHG emissions electricity and reductant fuel sources (steelmaking coal, natural gas and low to zero GHG emissions hydrogen) and technological advances.

These factors will determine how extensively hydrogen, natural gas, carbon capture, utilisation and storage (CCUS) and electrolysis are used in steelmaking.

A feasible GHG emissions intensity reduction trajectory for steelmaking is likely to involve a combination of existing blast furnace assets (modified to reduce their GHG emission intensities through technology such as carbon capture and storage), as well as the progressive introduction of other near zero emission process routes such as the EAF or ESF.

There currently are no near zero emissions technologies for iron ore-based steelmaking that are ready for widespread commercial adoption. This must change for us to achieve our long-term goal of net zero Scope 3 GHG emissions by CY2050.

Doing our part to support decarbonisation in steelmaking

Our strategy is to support the research and development of technologies across all four process routes.

Our program includes collaborative partnerships and consortiums that focus on developing and executing high-impact tests, trials, pilots and demonstrations that can be shared with steelmakers. These partnerships are in addition to research programs focussed on the fundamentals of decarbonisation technology for the sector, and investments in early-stage technologies with breakthrough potential via our dedicated Ventures team.

With around US$140m in funding committed by BHP from FY2020 to FY2024 and an estimated US$75m in additional funding planned for FY2025 to FY2029 (including BHP Ventures investments), we leverage our own funding to attract and enable investment (financial and in-kind) from our strategic partners.

We estimate a potential total co-investment figure of US$420M that could go into supporting the development of technologies across all four process routes. This figure combines our own funding (outlined above) with funding and in-kind contributions from our partners for the period from financial year 2020 to financial year 2029, creating insights across the potential technology pathways which may represent great value to the industry.

From the valuable insights created through pilot and demonstration projects that BHP and other industry participants are progressing over coming years, we expect the level of investment by the steel industry in the potential technology pathways to significantly increase as lower-carbon steelmaking options become more widely available after 2030.

We have 50 separate partners, including eleven steelmakers, 16 research institutes and 12 technology companies (both start-ups and vendors). Collectively, the eleven steelmakers that we are working with represent around 22 per cent of the world’s reported steel production.

For the blast furnace route, near zero emissions steelmaking options for the traditional blast furnace require CCUS in combination with other complementary technologies (e.g. top gas recycling).

The steel industry regards CCUS as a key abatement option for existing blast furnaces, and nine out of 10 of the largest steel producers who have set a net zero goal or target include CCUS in their roadmaps.

An example of our work to trial potential improvements for the emissions intensity of the blast furnace is our partnership with ArcelorMittal, Mitsubishi Heavy Industries and Mitsubishi Development. Together, we have designed, constructed and commissioned industrial pilot equipment at ArcelorMittal’s Ghent steelworks in Belgium, and will conduct testing for the next 12 to 18 months, including testing of other on-site GHG emission point sources.

For the two DRI process routes (DRI-EAF and DRI-ESF), the focus of our trials and pilot projects will be to demonstrate the use of our iron ores in each of the various process steps.

With DRI, hydrogen has the potential to decarbonise DRI to near zero emissions. One of our aims therefore is to establish and optimise the performance of our ores. For example, we are seeing growing use of our ores in pelletising in China and have recently commenced DRI production trials with two customers in China.

The DRI-EAF route is comparatively mature but lacks flexibility, with only between 3 and 4 per cent of global seaborne iron ore supply able to meet the specifications currently accepted in the market for production of DRI for EAFs. So, it is critical the steel sector seeks to develop alternative technology pathways to near zero emissions steel that may be more compatible with a wider range of iron ore types. This is where ESF is likely to become important.

To optimise the ESF process step, we need a deeper understanding of how DRI feed materials, based on our Pilbara ores, interact with ESF operational parameters to produce iron at the quality and productivity needed for downstream steel.

We have been establishing collaborative partnerships and consortiums for laboratory studies and pilot scale testing, and together with Rio Tinto and BlueScope we are working towards a pilot-scale facility to seek to resolve technical questions that cannot be answered in the laboratory.

This study is expected to conclude in FY2025. If approved, the pilot facility could be commissioned as early as CY2027.

Finally, to investigate the viability of electrolysis or electrochemical reduction (the fourth potential steelmaking process route), BHP Ventures has invested in electrochemical reduction technologies which have the potential to be transformative by utilising electrons instead of carbon to reduce iron oxide ores to metallic iron.

Leading startups Boston Metal and Electra have been demonstrating to us their focus to rapidly advance and adapt their technologies toward the technical demands of efficient, scalable iron and steelmaking. These technologies have now progressed through from the laboratory to pilot-scale, with plans for demonstration-scale options.

By investing in these different process pathways, we aim to help accelerate the development of technology that could have potential not only to reduce GHG emissions in our value chain, but also those of the broader industry.

1 Global steel production sourced from World Steel in Figures 2024, World Steel Association.

2 Funding committed by BHP in the past five years is made up our investments and contractual funding commitments for our steelmaking decarbonisation program from FY2020 to FY2024, including BHP Venture investments, research and development funding and collaborative partnerships (such as with our steelmaking customers).

3 0.40 tonnes of CO2-e per tonne of crude steel for 100 per cent ore-based production (no scrap), as defined by the International Energy Agency (IEA) and implemented in ResponsibleSteel International Standard V2.0 (‘near zero’ performance level 4 threshold). IEA (2022), Achieving Net Zero Heavy Industry Sectors in G7 Members, IEA, Paris, License: CC BY 4.0, which also describes the boundary for the emissions intensity calculation (including in relation to upstream emissions).