Potash: The Fourth Wave

Please refer to the Important Notice at the end of this article

At our potash briefing in June 2021, we introduced a long-run framework that not only neatly encapsulates the post-World War II history of the potash industry1 – it also offers a sensible guide as to what might lie ahead. We identified three major historical waves and speculated that the conditions that we saw unfolding just prior to the commencement of the Ukraine conflict marked the beginnings of a fourth. Given what we know about the fundamental inheritances of the industry, we predicted that the fourth wave may see more orderly demand and supply dynamics than the pattern observed in prior waves, where enduring imbalances were evident. A steady progression towards a relatively settled inducement pricing regime over the course of the 2020s was derived as the most likely outcome.

The dramatic volatility seen in the industry since that time has not dissuaded us from our long-term strategic position – indeed, our level of conviction has increased.

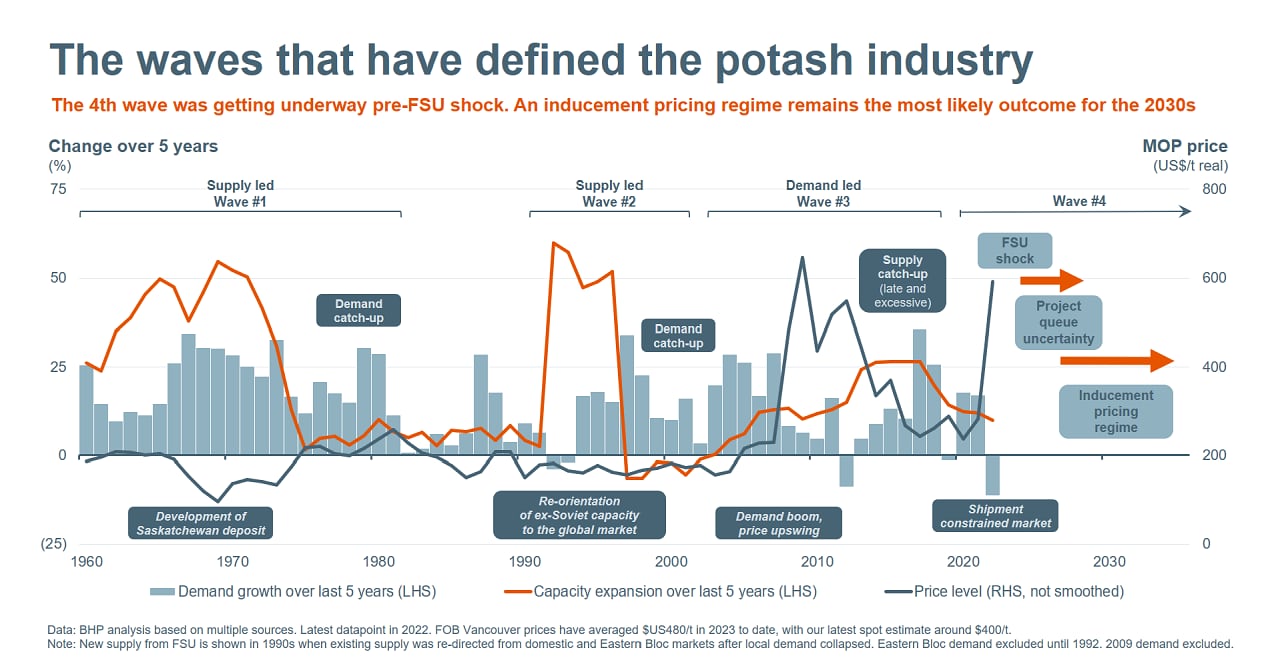

Figure 1 is a visual expression of our wave framework, updated since our June 2021 briefing. The columns and the orange line represent 5-year changes in demand and supply respectively, while the blue line is price (not smoothed).

Figure 1.

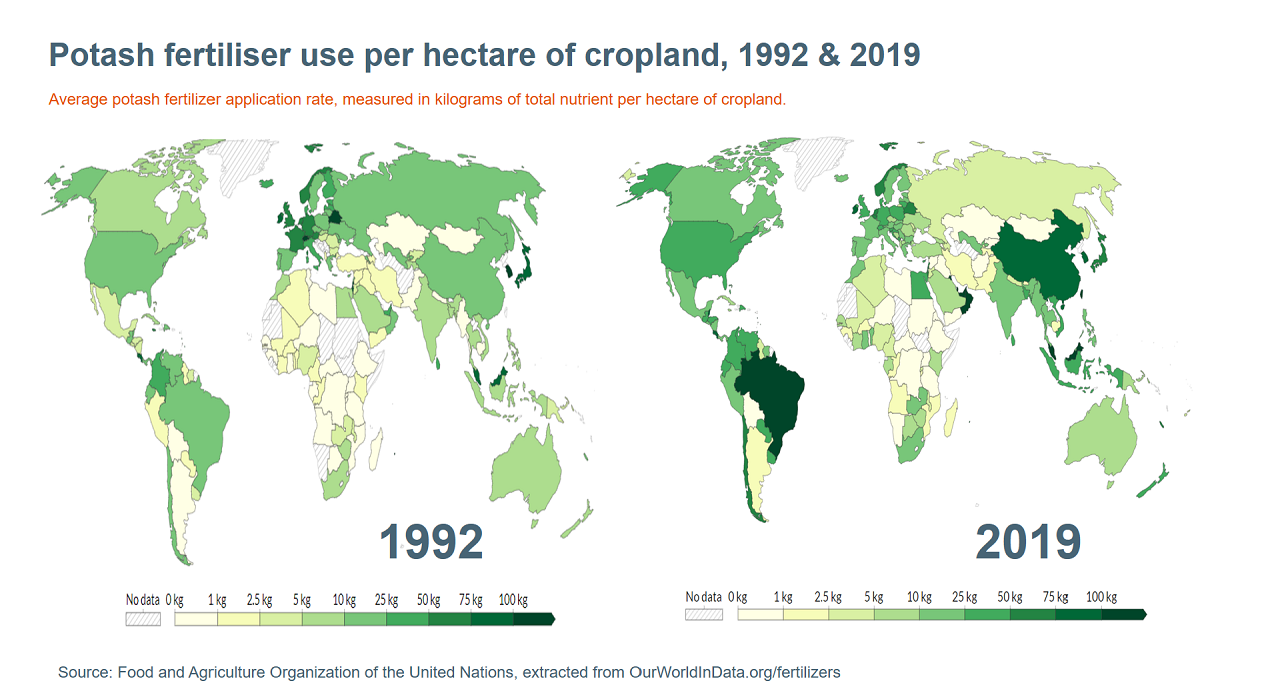

The last forty years of the 20th century comprised two waves, both of which were associated with major supply impulses. The 1st wave featured the opening of the enormous Saskatchewan basin in Canada, which is home to large industry incumbents Nutrien and Mosaic today. During this period, supply growth consistently outpaced demand, with a sustained period of depressed prices being the result. It took two decades for demand to completely catch-up, with the Green Revolution2 in the developing world an endogenous factor in this process. The 2nd major wave was defined by the disruptive re-orientation of former Soviet Union (FSU) capacity into the global market, after the collapse of the USSR. The influx of relatively low-cost FSU capacity created a glut in the global trade, with prices staying at or below short run marginal cost (SRMC) as the overhang was slowly absorbed. As figure 2 below illustrates, as global market access for the FSU region opened up, domestic application rates in the FSU went down in the following decades (the lighter shade of green in the map on the right vis-à-vis the left) and global application rates went up – a lot (the darker green on the right evident across China, South and Southeast Asia, North and South America).

Figure 2.

Following the two major supply impulses from Canada and then the FSU, the 3rd wave notionally started around the turn of the millennium, alongside the energy and metals super-cycles. Demand growth outpaced capacity expansions for multiple years in succession in the 2000s. The Global Financial Crisis (GFC) in 2008-09 proved to be a temporary hiccup, with demand again rebounding strongly in the early 2010s. The sustained demand upswing forced producers into catch-up mode for the first time since the opening of the Saskatchewan basin. A double peak of what we term “fly-up prices” [i.e. a price level without a stable fundamental basis in terms of the observable cost of operating supply – also known as “off cost curve” pricing] formed either side of the GFC. The supply response to this sustained period of attractive prices (which we note dragged forecasts of longer-term prices by specialist consultants up to eye watering levels) drew in the vast majority of the attractive brown and greenfield options remaining in the major basins – with the exception of BHP’s holdings of course. Over the five years to 2015, capacity grew by almost one-quarter. When demand growth came back down to more sedate levels, partly in response to the deterioration of affordability over the super-cycle phase, some of these expansions became regret decisions. The second half of the 2010s was characterised by an overhang of excess capacity, with assets voluntarily idled at this time to match the lower-than-expected demand. And that concluded the 3rd wave.

At our potash briefing in June 2021, we put forward a case that despite the difficulties of the last half-decade, the potash industry was becoming increasingly fundamentally prone to fly-up pricing. We also signalled what we thought future fly-up episodes might look like in terms of realised prices for producers.

Remarkably, within months of that presentation, and post our decision to reach a final investment decision on Jansen stage 1, a fly-up episode began to unfold. After a weak year for demand in calendar 2019, there was a strong rebound across calendar 2020 and 2021, and online assets did not, or could not, respond in lockstep (noting that a material portion of capacity was still latent at this time, a hangover from the late 2010s). Prices accordingly began to move quite rapidly, especially in the Americas. And then, just as prices looked to be fatiguing at high levels towards the end of calendar 2021, Belaruskali lost access to its key export port in Lithuania3, putting a question mark on the status of roughly one-fifth of internationally traded supply. Soon after, an already skittish industry was confronted with the commencement of the Russia-Ukraine conflict and a spike in global food prices that boosted farm economics. With the US and EU enacting far-reaching economic sanctions on Russia in response, including expulsion from the SWIFT international payments system, the question of what would come next cast considerable uncertainty over prompt supply availability from Russia. Potash buyers were understandably alarmed, with anxiety multiplied by the fact that there was very little buffer in the system after a stock rundown in 2021, and robust demand conditions were already stretching existing supply prior to these twin FSU shocks.

Some buyers, notably in Brazil and the US, responded by precautionary stocking, essentially “hoarding” potash in warehouses as a hedge against a sudden stop in availability. Consequently, prices moved beyond fly-up levels to a rare “scarcity regime”, with spot regional benchmarks nearing or exceeding historic highs, supported (for a time) by a corresponding upswing in crop prices. With profound uncertainty hanging over the future of supply from Belarus and Russia, some non-FSU producers also mobilised some idled capacity and announced medium term plans to expand capacity.

The old saying that “the best cure for high prices is high prices” is very pertinent in potash.

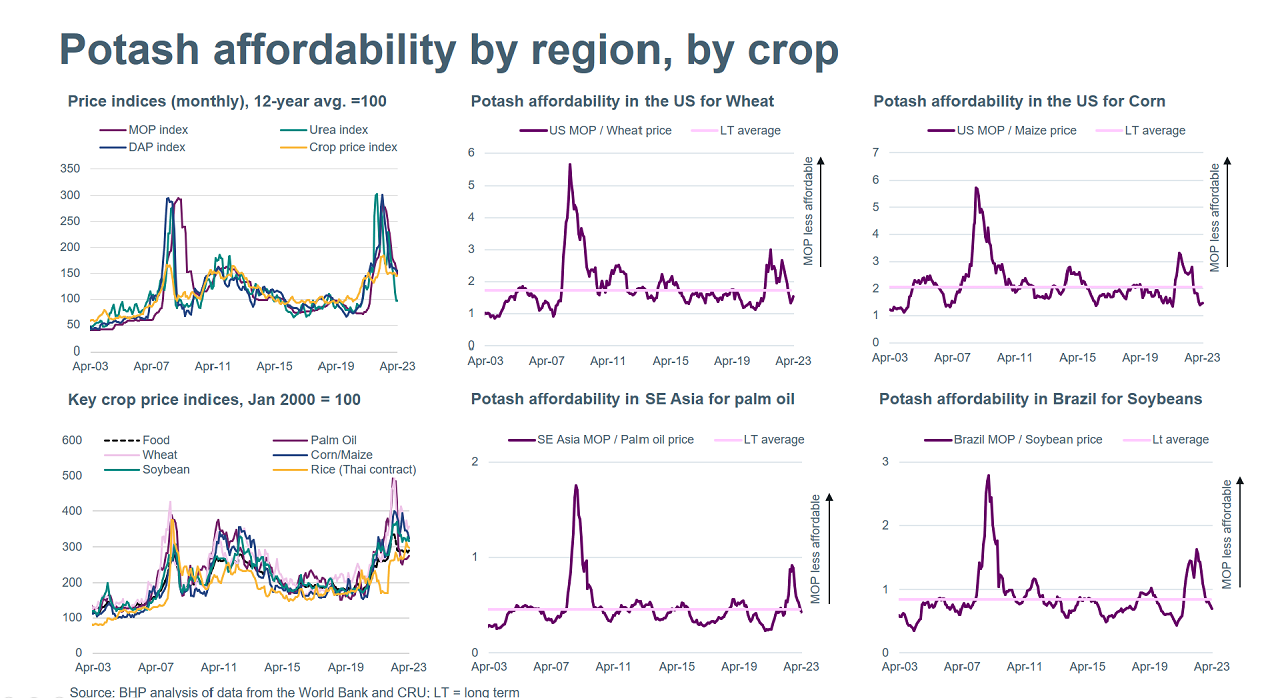

Contrary to metals and other bulk commodities, the cure can come quickly. In metals, once demand jumps out materially in front of supply, it can be a multi-year to decade-long process for new supply to bring the market to balance (depending upon the level of conviction in the deficit and the type of development options the industry is facing ex ante). In potash, the adjustment can come almost immediately: not via new supply, but via a buyers’ strike (aka potash holidays) as farmers reason that they can skip a season and get roughly the nutrients they need from “mining” the soil and recycling of crop residues and manures. This is exactly the bet that many farmers took in the second half of calendar 2022 once it became clear that the rally in crop prices was roughly half the scale of the rally in fertilisers, including MOP (the major bulk product within the potassium universe). Demand simply hit an air pocket. Import volumes in key spot regions like Brazil, the US and SE Asia declined sharply. Accordingly, non-FSU suppliers began to introduce soft curtailments in the December quarter of 2022 and started to soft-pedal on medium-term growth objectives. So, an industry that was expected to be supply constrained for most of calendar year 2022 closed the period constrained by demand as well: albeit major regional MOP-crop intersections were back closer to balance versus the long run affordability trend (see Figure 3 below).

Figure 3.

So what has recent history taught us about how the 4th wave might play out over the next two decades or so?

Prior to the twin FSU supply shocks, our view was clear: the potash industry was likely to absorb excess capacity and committed new supply (mostly from the FSU) by the late 2020s or early 2030s, with new greenfield supply required in that window. It also assumed that latent capacity, which is concentrated in Canada, would be mobilised in advance of the balance point – as otherwise it would be a faux equilibrium. Beyond the balance point, the most likely outcome seemed to be a durable inducement pricing regime in the 2030s, with new supply steadily brought online to meet trend demand growth, rather than aggressively pre-empting it.

How has our view changed? The first point is that even before we start to think about projects, existing capacity in the FSU still has work to do to return to normal operating and shipment rates, particularly in Belarus. It seems reasonable to assume that the first questions for Belarus will be re-establishing logistics routes (well advanced) and stabilising the operations themselves (a question on which we have limited line of sight). Only then might decision makers consider expansion plans (noting that the next replacement mine is not required until the early 2030s, on our estimates). For Russia, export flows were better than generally expected over calendar 2022, with Brazil, Southeast Asia, China and the US all taking reasonable volumes. It was only Europe and India where Russian shipments really dried up (with the Indian situation the continuation of a longer trend, with aggressive marketing by Belarus having gained them market share over time). With seemingly fewer issues moving and/or placing product than Belarus, it seems reasonable to assume that Russian project planning is somewhat more progressed. Even so, the prospective future removal of general sanctions seems an obvious signpost to watch in this regard – but as we move deeper into the second year of the Ukraine conflict, this does not feel imminent. Furthermore, availability of foreign financing, and perhaps even more importantly, access to foreign equipment (particularly European) may only return with a lag after general sanctions are removed. An alternative signpost would be the signing of substantial offtake agreements with friendly buyers to anchor prospective developments.

With Eurochem’s 2.3 Mt Volgakaliy mine now in production, the FSU pipeline features three ~2 Mt options: two in Russia and one in Belarus. The complexity of geopolitical dynamics in the FSU region lends itself to scenario analysis, not a hard-keyed central tendency, but as a starting point we think it is reasonable to conclude that these projects will be delayed by at least a few years from their currently announced schedules. We will come back to the implications of this potential delay in a moment.

Changing tack slightly, aside from being the world’s #2 supplier of potash (after Canada) Russia plays a pivotal role in international food supply chains. It contributes over 15% of total fertiliser exports globally, being #1 in nitrogen and #3 in phosphorus. Russia is also the largest exporter of wheat and is the biggest supplier into North Africa and the Middle East, where wheat is the staple grain. It is a major exporter of a range of other food products.

In addition to the top-down geopolitical headwinds impacting on the FSU food value chain, at the industry level, Russia has imposed several fertiliser and grain export curbs in recent times, constraining product flow and distorting supply chains. Spasmodic flows of chemical macro-nutrients from a top supplier hurts agricultural yields, drives a deterioration in both food affordability (for households) and fertiliser affordability (for farmers), and contributes to a food access and availability challenge for regions dependent on imports. While our monitoring of internet search traffic4 indicates that the very worst scenarios for food have not come to pass, partly due to the Black Sea grain export deals, some of the stress that was placed on the supply chain was obviously unnecessary.

The aforementioned chain of events, allied to the fact that Ukraine is also a major wheat, grain and oilseeds exporter, plus adverse weather and labour shortages, brought the issue of global food security to the fore once again in 2022: with some drawing parallels to the last major food crisis of 2007-08. We first wrote on the food (in)security topic back in 2019. How will the potash value chain respond to this latest reminder of the potential fragility of fertiliser and food supply? The first likely response is that an even greater value is going to be placed on reliability of suppliers: which is something we hear across our diverse businesses from all our customers. It is also possible that once supply conditions normalise, fertiliser importing regions will systematically target higher levels of inventory (both within the value chain and in strategic sovereign reserves) than they would have held in the pre-Ukraine world.

If this hypothesis eventuates, once the current constraints on product availability are surmounted, we might expect to observe a modest premium over trend demand emerge while the industry builds towards the new norm of higher precautionary stock levels as the decade extends.

Coming back to the point on the projected timing of a return to structural market balance, given potential delays to new FSU projects, an earlier balance point is certainly plausible. These dynamics also create the possibility of an earlier mobilisation of latent capacity by non-FSU producers; the advancement of some other “uncommitted” projects in the inducement queue; or some combination of the above. The pace at which regional demand will rebound adds further complexity to this equation. Any number of permutations of the above could plausibly ensue. We have expressed this as “project queue uncertainty” in Figure 1. The anchoring here comes from the fundamental premise that the market will need more primary supply once today’s current and projected excess capacity is absorbed, and that could happen as early as the third quarter of the 2020s, or as late as the first quarter of the 2030s. Pre the FSU shock, we felt that timing risks were balanced around the midpoint of that range. Post the FSU shock, there is a skew: we now consider that timing risks within the range are now tilted towards an earlier balance.

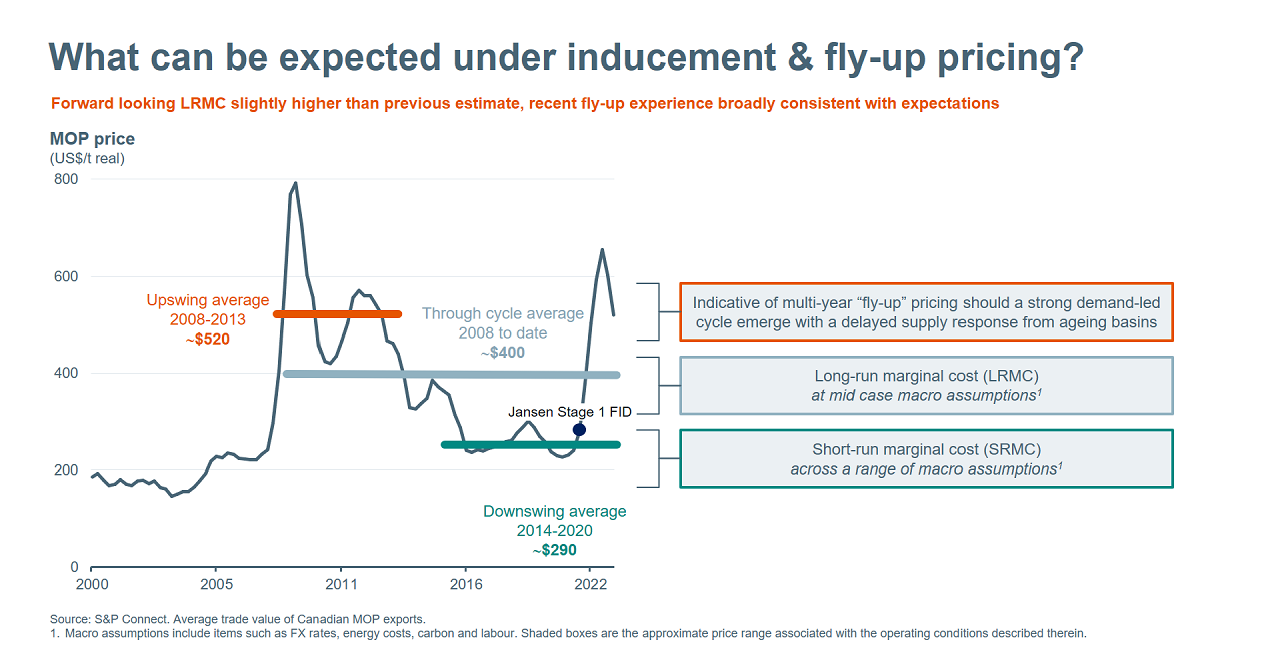

Besides our own decision to approve Jansen stage 1, which as mentioned above we took counter-cyclically before prices began to fly-up (see Figure 4 below), no big new potash mines have been announced in the major basins, and expansion plans outside the FSU have been medium-term, somewhat imprecise from an asset perspective, and conditional on the evolution of the external environment, rather than fully committed. Together, these observations are highly significant, as they are consistent with two salient expected features that we have ascribed to the 4th wave:

- There is a shortage of attractive conventional (as opposed to solution mining) development opportunities in the mature basins (ex BHP).

- A more disciplined approach to expansion under prospective fly-up pricing can be expected, heeding the lessons of prior waves that left a legacy of cyclical excess capacity.

The first point relies on the fact that most of the low cost, conventional brownfield and greenfield opportunities have already been prioritised for development. In bulk mining, you do not save the best for last. Outside of Canada and the FSU, operating assets in Germany and China, which collectively account for 14% of global supply (but not exports, with China producing ~7 Mt that is consumed domestically) are mature with a general lack of optionality. About 9% comes from the Dead Sea precinct, but there has been no growth signalling from that quarter. In Latin American brines, a combination of competition with lithium and water stewardship issues have seen production fall off. And there is a depletion challenge in the FSU beyond the 2020s.

On the second point, we have described the same essential concept previously as a “durable inducement pricing regime”. This has been expected to centre on a wide “bench” of potential solution mines in the southern part of the Saskatchewan basin in Canada. Relative to conventional mines, solution mines tend to have higher opex and require more sustaining capex. From a sustainability perspective, they also consume more water and energy. We estimate that a price in the high $300/t to low $400/t would be required to incentivise a material portion of Canada’s solution mines into production – similar to the through-cycle trend price for MOP. That is slightly higher than our estimate at the time of the Jansen stage 1 decision, reflecting both re-basing effects and higher carbon price assumptions.

Figure 4.

In a world where carbon pricing becomes more pervasive, the operating cost advantages of conventional mining should amplify, steepening the operating and inducement cost curves.

Undeniably, prices will continue to fluctuate – sometimes driven down to the SRMC, sometimes flying-up as the dynamics we have identified above periodically manifest. On a structural basis though, given the growing size of the market and corresponding resource availability, it is unlikely that the industry will return to the conditions we saw in the second half of the 20th century. You can only open a basin once.

Given these attractive fundamentals, it is strategically prudent for us to accelerate studies of our own capital-efficient organic options beyond Jansen Stage 1.

Important Notice

This article may contain forward–looking statements, including regarding trends in the economic outlook, commodity prices and currency exchange rates; supply and demand for commodities; plans, strategies, and objectives of management; assumed long–term scenarios; potential global responses to climate change; and the potential effect of possible future events on the value of the BHP portfolio. Forward–looking statements may be identified by the use of terminology, including, but not limited to , “intend”, “aim”, “project”, “see”, “anticipate”, “estimate”, “plan”, “objective”, “believe”, “expect”, “commit”, “may”, “should”, “need”, “must”, “will’, “would”, “continue”, “forecast”, “guidance”, “trend” or similar words, and are based on the information available as at the date of this article and/or the date of BHP’s scenario analysis processes. There are inherent limitations with scenario analysis, and it is difficult to predict which, if any, of the scenarios might eventuate. Scenarios do not constitute definitive outcomes for us. Scenario analysis relies on assumptions that may or may not be, or prove to be, correct and may or may not eventuate, and scenarios may be impacted by additional factors to the assumptions disclosed. Additionally, forward–looking statements are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties, and other factors, many of which are beyond our control, and which may cause actual results to differ materially from those expressed in the statements contained in this article. BHP cautions against reliance on any forward–looking statements, including in light of the current economic climate and the significant volatility, uncertainty and disruption arising in connection with the Ukraine conflict and COVID–19. Except as required by applicable regulations or by law, BHP does not undertake to publicly update or review any forward–looking statements, whether as a result of new information or future events. Past performance cannot be relied on as a guide to future performance.

Footnotes:

1 The pre-World War II history is also fascinating, but it is not particularly influential for the present, beyond the fact that the German mines that led global supply at this time are either retired or are approaching end of life, and replacing them will require new investment, likely in other regions.

2 The Green Revolution was the (almost) synchronised uplift in agricultural productivity across Asia and Latin America from the early 1960s, which allowed these populous regions to progressively break free of the famine cycle for the first time. The diffusion of improved techniques, fertilisers and pesticides were all essential inputs.

3 This even was pre-dated by the imposition of general sanctions on the Belarusian economy and various Belarusian nationals by the EU and US, with first actions by the EU taken in October 2020.

4 Google Trends, search item "food crisis" from 2004 to present.