Climate change

We believe warming of the climate is unequivocal, the human influence is clear and physical climate-related impacts are unavoidable. We recognise the role we play in supporting the net zero transition the world must make.

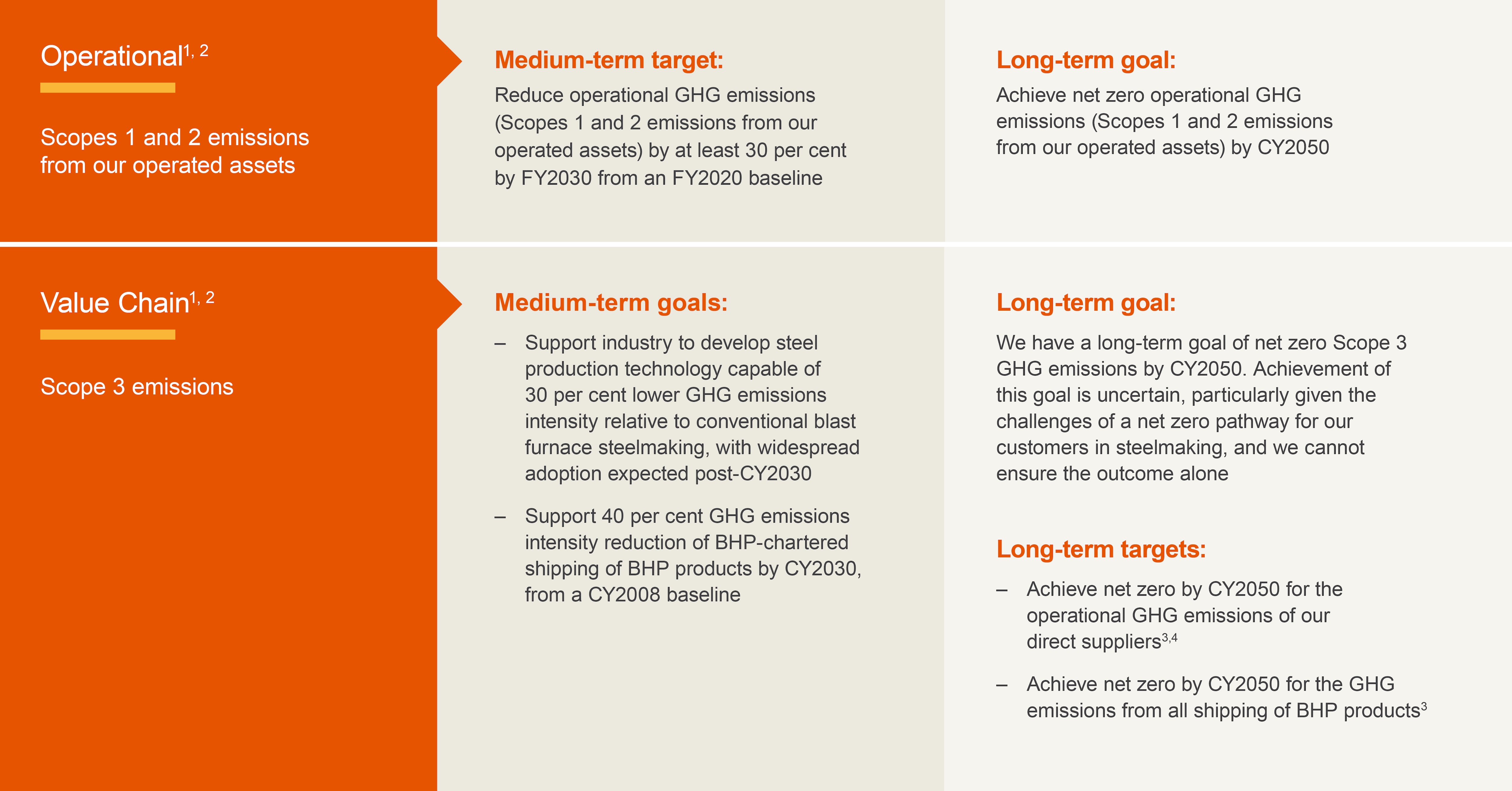

Our greenhouse gas emissions (GHG) emissions targets and goals

Notes and definitions

Information is valid at August 2025

- The baseline year, reference year and performance data of our GHG emissions targets and goals will be adjusted for any material acquisitions and divestments, and to reflect progressive refinement of GHG emissions reporting methodologies.

- Our operational GHG emissions medium-term target is referrable to an FY2020 baseline year and all our other targets and goals are referrable to a FY2020 reference year, except that our medium-term goal for shipping is referrable to a CY2008 baseline (which was selected to align with the base year for the International Maritime Organisation’s CY2030 emission intensity goal and its corresponding reasoning and strategy). The boundary of each target and goal may, in some cases, differ from required reporting boundaries. The use of carbon credits will be governed by BHP’s approach to offsetting, available at bhp.com/climate.

- Our ability to achieve the target is subject to the widespread availability of carbon neutral solutions to meet our requirements, including low to zero GHG emission technologies, fuels, goods and services.

- Operational GHG emissions of our direct suppliers means the Scopes 1 and 2 emissions of our direct suppliers included in BHP’s Scope 3 reporting categories of: Category 1, Purchased goods and services (including capital goods); Category 3, Fuel- and energy-related activities, Category 6, Business travel; and Category 7, Employee commuting.

- Baseline/baseline year (in relation to GHG emissions targets and goals): A year used as a basis to compare and measure performance of future years.

- Carbon credit: The reduction or removal of carbon dioxide, or the equivalent amount of a different GHG, using a process that measures, tracks and captures GHGs to compensate for an entity’s GHG emissions emitted elsewhere. Credits may be generated through projects in which GHG emissions are avoided, reduced, removed from the atmosphere or permanently stored (sequestration). Carbon credits are generally created and independently verified in accordance with either a voluntary program or under a regulatory program. The purchaser of a carbon credit can ‘retire’ or ‘surrender’ it to claim the underlying reduction towards their own GHG emissions reduction targets or goals or to meet legal obligations, which is also referred to as carbon offsetting or offsetting. We define regulatory carbon credits to mean carbon credits used to offset GHG emissions for regulatory compliance in our operational locations (such as the Safeguard Mechanism in Australia). We define voluntary carbon credits to mean carbon credits generated through projects that reduce or remove GHG emissions outside the scope of regulatory compliance (including Australian Carbon Credit Units not used for regulatory compliance).

- Carbon neutral: Making or resulting in no net release of GHG emissions into the atmosphere, including as a result of offsetting. Carbon neutral includes all those GHG emissions as defined for BHP reporting purposes.

- Goal (for BHP with respect to GHG emissions): An ambition to seek an outcome for which there is no current pathway(s), but for which efforts are being made or will be pursued towards addressing that challenge, subject to certain assumptions or conditions. Such efforts may include the resolution of existing potential or emerging pathways.

- Greenhouse gas (GHG): For BHP reporting purposes, these are the aggregate anthropogenic carbon dioxide equivalent emissions of carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs) and sulphur hexafluoride (SF6). Nitrogen trifluoride (NF3) GHG emissions are currently not relevant for BHP reporting purposes.

- Low to zero GHG emission(s) (for shipping): Capable of between 81 per cent to 100 per cent lower GHG emissions intensity (gCO2 -e/joule) on a well-to-wake basis compared to conventional fossil fuels used in shipping.

- Low to zero GHG emission(s) (for energy products other than shipping fuels): Capable of between 90 per cent to 100 per cent lower GHG emissions intensity during generation and/or combustion (as applicable) compared to conventional fossil fuel generation and/or combustion.

- Net zero (for a BHP GHG emissions target, goal or pathway, or similar): Includes the use of carbon credits as governed by our approach to carbon offsetting, available at bhp.com/climate.

- Offsetting (in relation to GHG emissions): The use of carbon credits. Refer to the definition of carbon credit.

- Reference year (for a BHP GHG emissions target or goal): A year used to track progress towards GHG emissions targets and goals. It is not a baseline for GHG emissions targets and goals.

- Target (for BHP with respect to GHG emissions): An intended outcome in relation to which we have identified one or more pathways for delivery of that outcome, subject to certain assumptions or conditions.

Climate change and climate transition planning is a material governance and strategic issue for us, our Board and management as described in the BHP Annual Report 2025, Operating and Financial Review 9.2 – Sustainability governance.

The Board is responsible for the governance and oversight of climate change issues, including in relation to our strategic approach, risk management and public disclosures. The Board approves significant social, community and sustainability policies, including those related to climate change and public sustainability goals and targets, and oversees performance against our strategy, goals and targets.

The CEO and Executive Leadership Team execute sustainability-related policies and strategy approved by the Board and are accountable for performance and achievement of BHP’s sustainability-related commitments, targets and goals, including our climate change targets and goals.

Achieving the goals of the Paris Agreement will require supportive policy across jurisdictions, globally. We believe BHP can best support policy development by ensuring we meet our own GHG emissions targets, goals and strategies, continuing to make the case for the economic opportunities arising from the energy transition, and focusing on those policy areas where we are likely to have the greatest ability to influence change.

Policy advocacy

We are committed to conducting our advocacy on government climate policy (direct and indirect) consistent with the goals of the Paris Agreement. We translate this into action by using our Climate Policy Principles in how we advocate (direct) and how we encourage industry associations where we are a material member to advocate (indirect). More information on our approach to direct advocacy is available here, while we detail our approach to indirect advocacy here.

Shareholder engagement

We use a range of formal and informal communication channels to seek to understand and take into account the views of shareholders.

We engage with shareholders through results roadshows and other investor engagement meetings, including on key issues such as climate change, industry associations and social value. BHP also hosts live webcasts and Q&A sessions with our senior leaders for shareholders to directly ask questions of management, including on topics such as climate change and decarbonisation.

We also facilitate and encourage shareholder participation at our Annual General Meeting (AGM). The AGM provides an update for shareholders on our performance and offers an opportunity for shareholders to ask questions and vote.

We are committed to providing transparency over our climate-related governance, risks (threats and opportunities), strategy, commitments and GHG emissions targets and goals, enabled through regular disclosures.

We also recognise the importance of investors and other stakeholders being able to understand the potential impacts on BHP’s financial position from climate-related risks (threats and opportunities). In our Financial Statements in the BHP Annual Report 2025, we capture potential financial statement impacts, where material or relevant, of the assumptions, plans and actions of our climate change strategy and the consideration of climate-related risks in the assessment of significant areas of judgement and estimation required for the presentation of the financial statements.

Our most recent climate-related disclosures can be found in the:

- BHP Annual Report 2025, Operating and Financial Review 9.8 – Climate change

- BHP Annual Report 2025, Financial Statements – note 16 'Climate change'

- BHP Climate Transition Action Plan 2024, subject to updates of certain aspects of our assumptions and plans in the BHP Annual Report 2025, Operating and Financial Review 9.8 – Climate change

- BHP ESG Standards and Databook 2025

- BHP GHG Emissions Calculation Methodology 2025

Our most recent climate-related performance data can be found in the:

- BHP Annual Report 2025, Operating and Financial Review 9.8 – Climate change

- BHP ESG Standards and Databook 2025

BHP Insights and presentations

Sustainability case studies, organisational boundary, definitions and disclaimers, and downloads

-

BHP Annual Report 2025pdf

-

Sustainability reporting organisational boundary, definitions and disclaimerspdf

-

Límite organizativo de los informes de sostenibilidad, definiciones y descargos de responsabilidadpdf

-

BHP ESG Standards and Databook 2025xlsx

-

BHP Group Modern Slavery Statement 2025pdf

-

BHP GHG Emissions Calculation Methodology 2025pdf

-

BHP Climate Transition Action Plan 2024, subject to updates of certain aspects of our assumptions and plans in the BHP Annual Report 2025, Operating and Financial Review 9.8 – Climate changepdf

-

Global Industry Standard on Tailings Management - Public Disclosure 2025pdf

-

Tailings Storage Facility Policy Statement 2023pdf

-

Case studies