Pathways to decarbonisation episode one: power

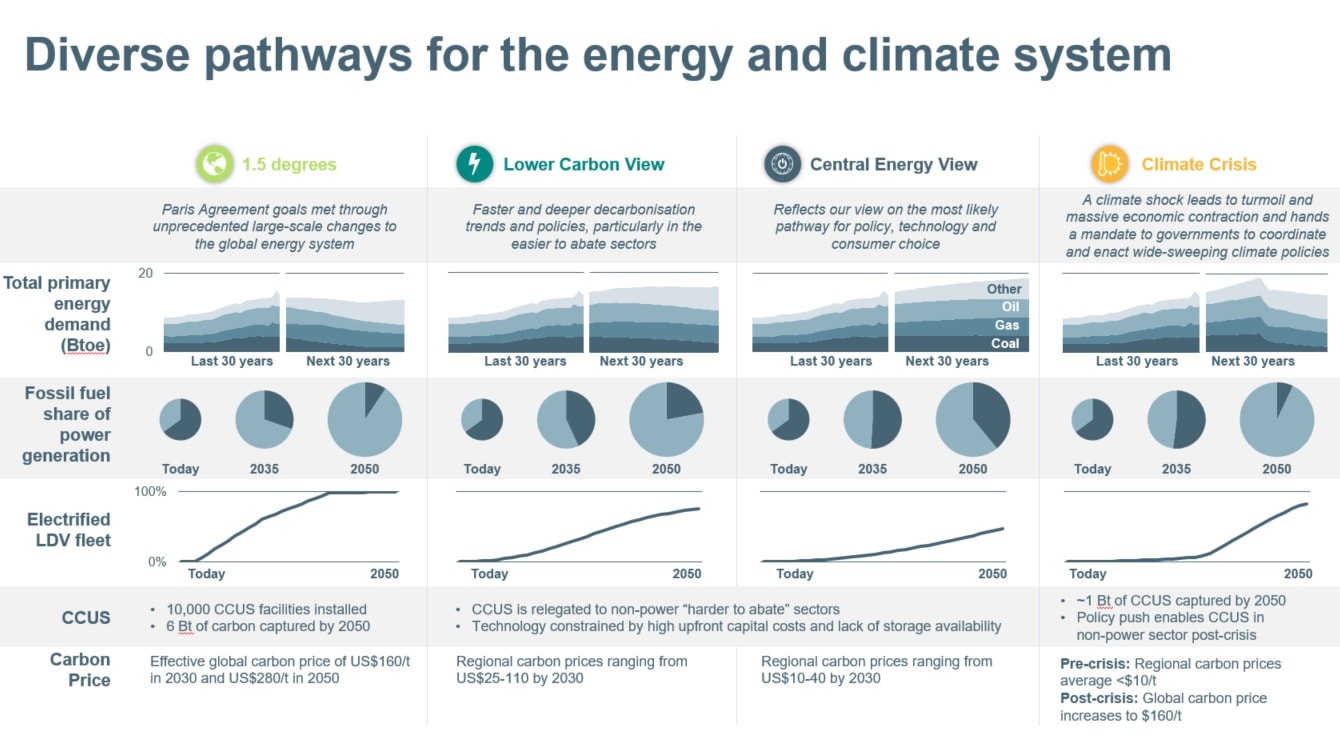

On September 10, we released our Climate Change Report 2020, following our initial “Climate Change: Portfolio Analysis” report in 2015 and “Views after Paris” in 2016. The latest update features two new scenarios. One is a Paris Agreement-aligned pathway, which tracks to 1.5 degrees Celsius of warming by 2100. The second is a dynamic, non-linear “Climate Crisis” scenario1. Taken together, they send three strong messages.

- Early and decisive global action to tackle climate change will benefit BHP’s overall portfolio.2

- To concurrently meet rising living standards and achieve wholesale decarbonisation, the resources sector needs to grow.

- The challenges for deep decarbonisation are immense.

Here we build on our analysis of the scenarios by diving into one of the essential questions in this field: how, and how fast, could stationary power decarbonise? This is the first episode in a series on decarbonisation, with steel decarbonisation coming next.

Any climate and energy system modeller knows that it’s one thing to run a technical scenario as an optimised lowest cost abatement exercise: and it is quite another to overlay the messiness of the real world. Most technical pathways ignore many complicated behavioural questions (temporal, regional, social, political) that drive investment and policy decisions. While technical pathways are useful to gauge what is possible, they may not always gauge what is plausible. That is why our (growing) scenario set comprises both technical and behavioural pathways, as well as hybrids of the two, underpinned by bottom-up sectoral simulation. We do not choose one over the other. At BHP, we do “clean”, we do “messy”, and many points in between.

Almost all Paris-aligned technical scenarios take decarbonisation of the “easier-to-abate” sectors—namely light duty transport and electricity—as a given. Our focus here is on electricity. Our aggressive views on electric vehicles are well known, and can be revisited in episode one, episode two and episode three of our Prospects series on the electrification of transport.

The stationary power sector, which today accounts for 40% of global CO2 emissions, must entirely decarbonise in the next three decades if the world is to stay within a 1.5 degree budget3. This is not just due to the emissions that must be abated from power generation; the sector’s growth also opens up large opportunities through the green electrification of other energy processes. It is the gateway to where the world needs to go.

Much has changed in the power sector over the last two decades. Solar costs have fallen by over 90% since 2008. Utility-scale batteries are being installed across the US, Australia and Europe. India has achieved 100% household electrification (on one set of estimates at least). Since its 2011 vintage of forecasts, the International Energy Agency has almost tripled its projection of solar and wind power generation in 2035. President Xi Jinping has announced an aim for China to reach net zero emissions by 2060. And yet, in big picture terms, much is still the same. Fossil fuels still represent almost two-thirds of electricity generation, and in 2019, net coal-fired capacity actually increased by +2% year on year. US$131 billion of additional investment flowed into new fossil plants just last year.4

So, if we start with the assumption that the world is able to replace two-thirds of the current generation mix (and still meet growing demand) so the resulting generation is nearly CO2 free by 2050, how do we get there?

We considered a wide range of pathways to reach this future state. The most plausible of them featured very deep renewables penetration. In short, we think that extremely rapid dissemination of wind, solar (depending on their relative competitiveness by geography) and eventually batteries is the most likely avenue if the world is to decarbonise in that time frame. The relatively low project risks of wind and solar projects, including their modular nature, strong policy support in many jurisdictions, steady technological progress and the ability to sustain rapid gains in manufacturing productivity, have created abundant opportunity for increased competitiveness. The solar industry, in particular, has leveraged manufacturing economies of scale to lower unit costs, while rapidly increasing the efficiency of solar cells.5

The progress made by wind and solar puts them well ahead of other low or zero emissions generation technologies — nuclear, carbon capture utilisation and storage (CCUS), tidal and wave technologies, among others — in the race to achieve cost parity with coal plants (in most regions) and gas plants (in the US). By the time these other technologies are projected to close the gap to the lowest cost fossil option in each region, that likely will no longer be the relevant benchmark: renewables will be.