BHPs economic and commodity outlook

Financial year 2021

20 August 2021

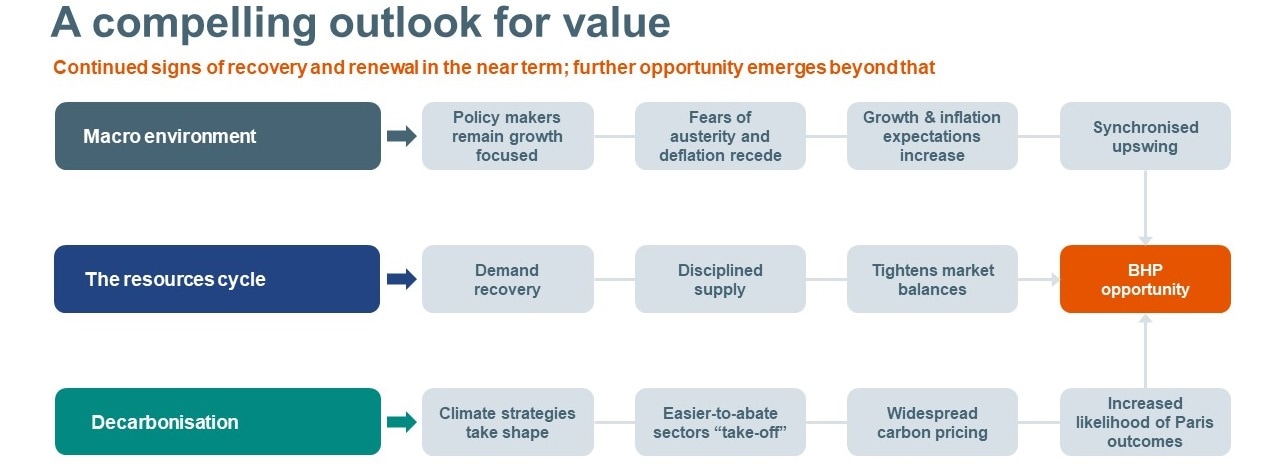

Six months ago1, at the time of our half year results for the 2021 financial year, we presented a constructive outlook for our commodities and for the world economy as a whole. At this time, some of our commodities were still facing a challenging environment in absolute terms, while others had entered a clear recovery phase for both demand and price. As we release full year results today, operating conditions for the majority of the portfolio have improved markedly, as anticipated. Most of our major commodities are now trading at prices that are close to, or above, our estimates of long term equilibrium.

For the 12 months ahead, we assess that weighted directional risks to prices across our diversified portfolio are steady. While some uncertainties remain, our base case is constructive.

We expect the demand–supply balance to remain relatively tight in both iron ore and copper. The balance of risks for oil prices are tilted modestly upwards. Metallurgical coal prices have rebounded, for now, on multi–regional supply disruptions and strong downstream conditions in the steel sector. Nickel demand is robust but supply is expected to keep pace. Potash is in the midst of a bull run, driven by strikingly positive downstream fundamentals at a time of constrained supply.

There is obviously still some residual uncertainty as to how vaccine deployment and the policy and behavioural response to the newer, more infectious strains of COVID–19 will interact over the coming quarters. There is also some nervousness in financial markets about the timing and extent of the eventual exit from loose global monetary policy. So while the “uncertainty discount” in the risk appetite of households and businesses we have noted in previous communications is definitely fading, it is doing so in uneven fashion across the world. That said, while the world’s two major systemic growth engines – the US and China – are performing strongly, there is probable cause for optimism that the rising tide can progressively lift all boats.

Looking beyond the immediate picture to the medium–term, we continue to see the need for additional supply, both new and replacement, to be induced across most of the sectors in which we operate.

After a multi–year period of adjustment in which demand rebalances and supply recalibrates to the unique circumstances created by the COVID–19 shock, we anticipate that higher–cost supply will be required to enter the cost curve in our preferred growth commodities as the decade proceeds.

COVID–19 has altered many things, but it does not alter geology or define the frontier of operational efficiency in each commodity sector. Besides demand, these are the two most critical factors for identifying marginal sources of long run supply: and what it will cost to bring those resources to market.

The steepening of some industry cost curves that we monitor, albeit delayed from prior expectations, can reasonably be expected to reward disciplined owner–operators with higher quality assets featuring embedded optionality.

In the medium and long term, on the demand side, we continue to see emerging Asia as an opportunity rich region. As the true costs of a partial retreat from economic openness and a lack of climate action are progressively recognised, we anticipate a popular mandate for a more open international trading environment will eventually re–emerge, along with a concerted effort to confront climate change as a basic imperative.

We note that the younger generations that will define our future – both Millennials and Generation Z – are not only more concerned about climate change than their elders in both East and West, they are also more favourably disposed towards globalisation.2

On that uplifting note, we confidently state that the basic elements of our positive long–term view remain in place.

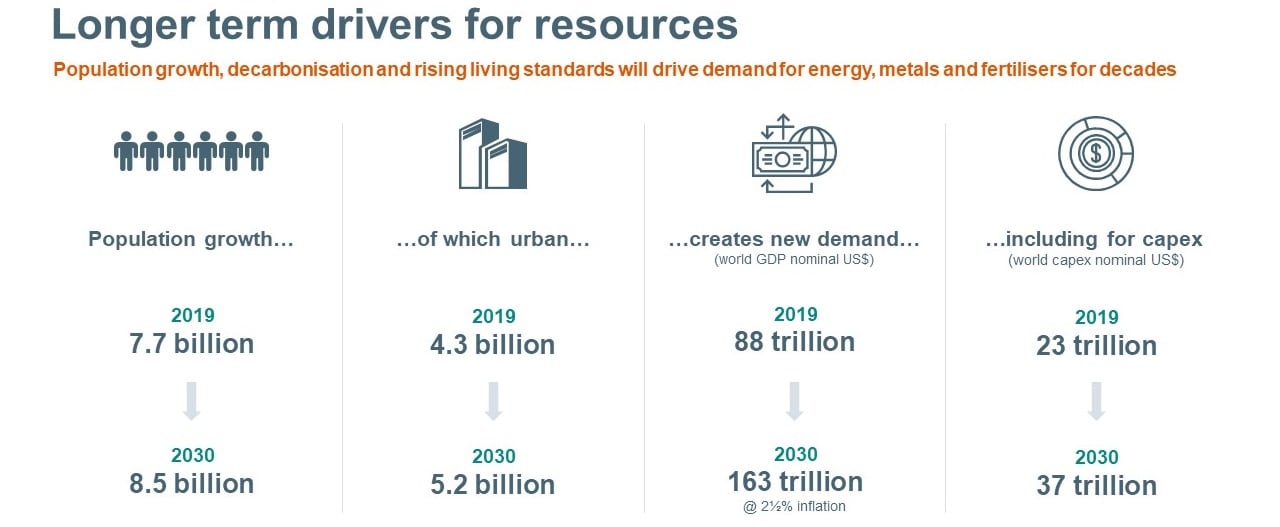

Population growth, the infrastructure of decarbonisation and rising living standards are all expected to drive demand for energy, metals and fertilisers for decades to come.

In the 2020s specifically, we expect global population to expand by 0.8 billion to 8.5 billion, urban population to also expand by 0.8 billion to 5.2 billion, nominal GDP to expand by $75 trillion to $163 trillion and capital spending to expand by $15 trillion to $37 trillion.3 Each of these basic fundamental indicators of resource demand are expected to increase by more in absolute terms than they did across the 2010s.

Furthermore, with fiscal and monetary policy makers in key economies committing themselves to a reflationary agenda, the secular fundamentals that make our industry attractive may be amplified. [see 4 for below]

We firmly believe that our industry needs to grow in order to build a better, Paris–aligned world.

The IPCC stated on August 9 that “Unless there are immediate and large-scale greenhouse gas emissions reductions, limiting warming to 1.5 degrees Celsius will be beyond reach”. As illustrated by the scenario analysis in our Climate Change Report (available at bhp.com/climate), if the world takes urgent actions to limit global warming to 1.5 degrees, we expect it to be advantageous for our portfolio.5 We note, of course, that there is an almost infinite array of technical, behavioural and policy assumptions that can achieve this end in combination, and our 1.5 degree scenario is just one of the many. Each unique pathway produces a unique call on commodity demand and presents a unique incentive matrix vis-a-vis supply. This highlights the need to avoid treating any single pathway as the source of “truth”. That is too heavy a burden for any one scenario to carry. As the common knowledge base of publically available Paris-aligned scenarios continues to grow, we will continue to learn from this invaluable collective resource to improve the work that helps to inform our strategic deliberations.

What is common across the vast majority of the 100 or so Paris-aligned pathways we have studied is that they cannot occur without an enormous uplift in the supply of critical minerals such as nickel and copper. And some of the scenarios we have studied, such as the International Energy Agency’s high profile Net Zero Emissions scenario6, would be even more favourable for our future-facing non-ferrous metals than what is implied by our own work to date: albeit with different assumptions and potential impacts elsewhere in our portfolio.

Now: add each of the constructive foregoing themes to the fact that the industry as a whole has been disciplined in its allocation of capital over the last half decade. With this disciplined historical supply backdrop as a starting point, any sustained demand surprise seems likely to flow almost directly to tighter market balances.

Investment that seeks to abate emissions and/or adapt to, insure against and mitigate the impacts of climate change are expected to rise to become a material element of demand for parts of our portfolio. The electrification of transport and the decarbonisation of stationary power are expected to progress rapidly, and the desire to tackle harder–to–abate emissions elsewhere in the energy, industrial and land–use systems is building. Comprehensive stewardship of the biosphere and ethical end–to–end supply chains will become even more important for earning and retaining community and investor trust.7

The ability to provide and demonstrate social value to our operational and customer communities is both a core enabler of our strategy and a source of competitive advantage.

Against that backdrop, we are confident we have the right assets in the right commodities in the right jurisdictions, with attractive optionality, with demand diversified by end–use sector and geography, allied to the right social value proposition.

Even so, we remain alert to opportunities to expand our suite of options in attractive commodities that will perform well in the world we face today, and will remain resilient to, or prosper in, the world we expect to face tomorrow.

Table of contents

Global economic growth

The world economy contracted by –3.2% in calendar year 2020. We anticipate an outcome comfortably above +6% in calendar 2021. We now estimate that the world economy will be 4% smaller in the 2021 calendar year than it would have been if COVID–19 had not occurred: ½% stronger than our view of six months ago.

The difference reflects the speed of the rebound in developed countries in the calendar year to date, led by the US, as well as better than expected performances across the emerging world, especially those regions positively leveraged to the commodity price upswing. India’s most recent COVID–19 wave has made it a notable exception to the improving trend in recent quarters. The Chinese economy has met our above–consensus expectations. Against this backdrop, exchange rates have been somewhat volatile, but compared to the levels prevailing at the time of our half–year results, the US dollar index (DXY) was largely unchanged as the financial year 2021 closed. In real trade weighted terms, as of June 2021 the US dollar had declined by roughly –8% from the recent peak achieved during the COVID–19 panic of April 2020.

The volume of global trade growth collapsed by –8.3% in calendar 2020. A very strong recovery is now underway, with Jan–May 2021 data showing growth of 14.0% year–to–date YoY. As of May 2021, the volume of world trade was 4% above calendar 2019 levels. Exports from developing economies are 8% above 2019 (China 18%) and exports of developed countries are up 1% on the same basis.

Unit prices of world exports are up 10% on the calendar 2019 level.

As global policymakers shift their attention from cushioning the impact of COVID–19 to either actively spurring recovery or calibrating a delicate exit from today’s extraordinary policy settings, it is worth recalling that the underwhelming performance of the global economy in calendar year 2019 was in large part due to weak international trade and the associated negative impacts on business confidence.

Trade is the essential lubricant of global economic growth, and a reflationary agenda ought to embrace that fact.

In addition, we strongly encourage policymakers to prioritise structural reforms at home as the surest route to sustainable productivity growth, and ultimately, prosperity, coming out of COVID–19.

Remaining open to the cross–border flow of people, goods, capital and ideas is vital to this end: free trade based on comparative advantage, competition, productivity and innovation are close companions.

These arguments highlight the importance of continued and vocal advocacy for free trade, open markets and high quality national and multilateral institutional design by corporations, governments and civil society.

A key feature of the global economic recovery in calendar 2021 to date has been a series of upside surprises in measures of economy–wide inflation, with upstream (PPI) readings particularly elevated.

Supply elasticity in a range of goods–producing and distributing sectors has fallen well behind the speed of the turnaround in demand. Triggered in part by upstream price appreciation, and in some cases spurred by constrained supply downstream, many of the world’s most essential end–to–end value chains – for example petroleum products, construction materials and food – and the associated distribution industries (principally land, sea and air logistics) are on the move. As of June 2021, consumer and producer prices in the US were tracking above 5% and 7% YoY respectively. The most recent updates on producer price inflation in the EU, Japan, China and India are distinctly elevated relative to regional norms, at 10.2%, 5.0%, 9.0% and 12.1% YoY respectively. Major commodity producing countries such as Chile, Canada, Brazil and Russia are seeing even higher outcomes. Australia is a low outlier in terms of producer price inflation at present (2.2% YoY in the June quarter, with consumer price inflation at 3.8% YoY).

Some aspects of the current global inflation uplift will obviously prove to be transitory as supply recalibrates over time and base effects reverse. Even so, we anticipate that average economy–wide inflation this decade will be higher than the last.

That is partly due to our constructive underlying view of world growth and the likely performance of the resources industry against that backdrop after a half decade (and counting) of disciplined capital allocation. This thesis also relies on the fact that policy makers are altering their medium–term strategies with respect to both monetary and fiscal policy in a way that is more accommodative of a moderate lift in inflation than the frameworks they are replacing. The impact on private sector confidence of this pro–growth policy stance will be positive and durable, in our view.

China’s economy traced a spectacular V–shape across calendar 2020, with strong momentum carrying over into calendar 2021. As of today the economy appears to be on a firm footing, with balanced contributions to growth coming from each of the key pillars of investment, the consumer and exports. The recent COVID–19 outbreak centred on Nanjing is an emerging risk to growth that we are monitoring closely.

Six months ago we argued that while in an absolute sense China has made a considerable effort to support jobs through the pandemic, in a relative sense policymakers have not over–stimulated.

That judgement gauges the Chinese response versus developed countries during the pandemic, and relative to its own actions in response to the GFC. Nothing that has occurred since has altered that opinion.

The performance of key minerals end–use sectors relative to our views six months ago has been a slightly mixed bag. Some have met expectations (real estate, conventional transport machinery) some have exceeded them (industrial machinery, electric vehicles, renewables infrastructure and consumer durables,) while traditional infrastructure has been a little disappointing. The weighted average has resulted in a slight positive surprise.

We anticipate that national level housing policies and rhetoric will remain directed towards limiting speculation, managing macro–prudential risks and building rental markets. The major influence on the market in coming years is expected to come from the supply side of the industry, with property developers managing their balance sheets within stricter new macro–prudential criteria. After many years of prioritising land acquisition and project origination, running up a large stock of real and contingent liabilities in the process, developers will likely have to give much greater emphasis to project completions in the period ahead to consolidate their balance sheets. That is expected to manifest in a multi–year outperformance of housing completions vis–à–vis starts: the opposite of the experience in this unusually protracted housing upswing to date. As this adjustment process plays out, the historical lead–lag relationships that exist between the four key fundamental floor space parameters (sales/starts/completions/under construction) are expected to be somewhat less reliable than in the past.

As of June 2021, the volume of housing starts – the key indicator for contemporaneous steel use in real estate – is around 5% higher than in 2019, but –3.8% YoY. Sales volumes are up 10% and 7.5% on the same basis. The equivalent comparisons for housing completions – the key indicator for contemporaneous copper use in real estate – are 156% and 67%.

Auto production lagged other areas of manufacturing coming out of the COVID–19 trough due to supply chain issues. After a relatively short period of recovery, the supply chain is again serving as a constraint, with the global semiconductor shortage now artificially limiting production potential. However, this constraint has not been binding on electric vehicles (EVs), which have sprinted ahead in the first half of calendar 2021 with triple digit YoY percentage growth recorded in each of the first six months of the year. Machinery production has been very strong. All major segments have all seen material growth over pre-pandemic levels, with domestic and export demand both set to a favourable pitch. More recently, we have noted that infrastructure linked segments (excavators, power generating equipment) have come off the boil somewhat, while demand for manufacturing machinery (metal cutting tools, industrial robots) has remained robust.

On exports more generally, Chinese manufacturers have been arguably the leading beneficiaries of the global boom in goods consumption observed over the last 12 months. Exports were up by around 40% YoY in Jan-May 2021, versus the growth in world imports at around 13% YoY. When you are the world’s largest exporter of manufactured goods to begin with, it is very difficult to outgrow the global aggregate by such a wide margin. Over the longer term, our view remains that China’s economic growth rate should moderate as the working age population falls and the capital stock matures. China’s broad production structure is expected to continue to rebalance from industry to services and expenditure drivers are likely to shift from investment and exports towards consumption.

Nevertheless, China is expected to remain the largest incremental contributor to global industrial value–added and fixed investment activity through the 2020s even as its growth rates mature.

Within industry, we expect a concerted move up the manufacturing value–chain. This will require further improvements in the domestic innovation complex. Notwithstanding the natural emphasis now being placed on “dual circulation”8, given the times we live in, we anticipate that the concerted move outwards of recent years is likely to continue, with an emphasis on South–South cooperation, regional trade agreements9, and the Belt–and–Road corridors. More broadly, we anticipate environmental concerns will become an even more important consideration in future domestic and foreign policy design than they are today. Within this context, China’s plans to see emissions peak in advance of 2030 looks readily achievable, while hitting its net zero by 2060 objective is a considerably more challenging task.

Major advanced economies

The US has been the outstanding economic performer among the major developed economies. At the time of our half year results, fiscal support of around $3½ trillion had been committed and the Federal Reserve had expanded its balance sheet by around 15% of GDP. Fiscal announcements since that time take the prospective total to an astonishing $10 trillion, albeit with some risk that Congress does not pass the original packages in full. The Fed has also adopted a new “average inflation targeting” (AIT) framework that prioritises the pursuit of maximum employment: and to help accommodate that pursuit, periods where inflation is sustained above the historical 2% objective are now explicitly condoned. The Fed’s balance sheet has quietly expanded by an additional 3% of GDP in the meantime.

The practical application of the Fed’s new framework is undergoing its first test, with urban consumer price inflation and the personal consumption deflator exceeding 5% and 4% respectively in their latest readings.

We noted above that some aspects of the global inflation spike are almost certain to be transitory. Even so, in the US there are genuine fundamentals tailwinds for growth and employment – and by extension inflation – due to the robust strength of the real economy. These tailwinds feel as if they could persist for some time, with or without further impetus from fiscal policy. The housing market and business investment are both major activity bright spots. Total construction spending and durable goods orders (ex–aircraft) are both sitting at all–time highs in level terms. And the huge pool of excess savings on household balance sheets that we have emphasised previously have begun to be put to work. Total consumer expenditures are now almost $1 trillion higher than pre–pandemic levels, roughly half of which is attributable to a step wise increase in purchases of durable goods.10 As spending inevitably rotates back in the direction of services, there should be a boost for the labour market: with wages of course being the single most critical factor in any medium term forecast of aggregate inflationary pressures.

In the wake of the inauguration, six months ago we wrote that “The Biden administration is a pivotal one in global history:

- It has the potential to rapidly accelerate global decarbonisation trends.

- It faces monumental geopolitical choices, both in terms of its approach towards multilateralism and its attitude towards key bilateral relationships.

- It has the potential to re–set the prevailing macroeconomic policy orthodoxy.

Much depends on these choices, for the US itself and the world.”

In terms of signposts to date, we note that:

- In trade and foreign policy, there is continuity from the previous administration in terms of the determination to treat China as a rival, and to pursue a nationalistic line on trade more broadly. However, there have also been clear efforts to re–engage constructively with both immediate allies and with the multilateral architecture.

- Climate action has clearly entered into the Administration’s everyday domestic and foreign policy discourse, and

- The overriding commitment to reflating the economy and creating jobs is clear, with the White House, the Treasury and the Fed seemingly of one mind on this score.

In Europe and Developed Asia, the scale of recovery since the deep contractions of the June quarter of 2020 have been respectable viewed as an aggregate, but experientially it has felt quite stop–start, reflecting both additional waves of the pandemic and supply constraints in key sectors. Common to the US experience though, housing markets have picked up across Europe, Japan and South Korea, some upstream inflation is evident and manufacturing surveys imply generally favourable operating conditions.

In Developed Asia, Japan’s economy did not cope particularly well with the first phase of the pandemic, which hurt business confidence and left the supply side of the economy somewhat flat–footed as many of Japan’s trading partners were able to rapidly exit lockdowns in the September quarter of 2020. Japan’s exports of machinery and transport equipment – the core of its industrial economy – were stuck below year–ago levels essentially until after the end of the Lunar New Year 2021. Conditions have improved since, with the main constraints on a more aggressively positive outlook being the possibility of super–spreader event in the wake of the Olympic Games and the deleterious impact of the ongoing semiconductor shortage. South Korea has been somewhat more resilient throughout, containing its initial outbreak quite effectively while also benefitting from the observed improvement in the global electronics sector. South Korea’s semiconductor exports rose an impressive 34% YoY in June 2021, or 52% higher than in December 2019.

Europe has been neither a leader nor a laggard in terms of peer economic performance over the last 18 months, but as of the time of writing, it is enjoying something of a sweet spot. Higher frequency data suggest that European manufacturers enjoyed increasingly strong operating conditions over the first half of calendar year 2021. The pan–European PMI recorded four consecutive months above 60 from March through June, averaging 63 – the best performance among major economies globally. By way of comparison, the global average was 55.6, the US was 61, while Japan and South Korea averaged around 53 and 54 respectively. Consumer confidence and sentiment in the construction sector are also at multi–decade highs, and exports are rising strongly.

Against this promising short–run backdrop, the European Central Bank (ECB) revealed a new, more accommodative policy framework in July 2021. Following the release of the US Fed’s new strategy (as discussed above), the ECB’s response, which is arguably even more dovish than the Fed’s versus their historical reaction functions, is a major signpost that policy makers in systemically important regions are prioritising the reflation of their home economies above all else. The contrast to the “currency wars” and failed fiscal austerity of the 2010s is stark.

On a different note, we observe that European countries mobilised $166 billion of energy transition related investment in calendar 2020, more than the other two big spenders, China ($135 billion) or the US ($85 billion).11 With the draft proposals for the much awaited European Carbon Border Adjustment Mechanism now released, which is one of the flagship policies of the EU’s upgraded “Fit for 55” emissions reduction ambition by 2030 (versus a 1990 baseline), no region has been more active in the climate domain.12

India

India’s economy has been unusually hard to read in the pandemic era. With its distinctive combination of scale and volatility, it has become a major swing factor in short term forecasts of global growth.

Activity completely collapsed under the lockdown of the June quarter of 2020, with the scale of India’s contraction more than double what China experienced the quarter before. Then activity rebounded smartly from the nadir, and the second half of the calendar year ended up being quite good – and versus expectations, spectacularly good. Therefore, as forecasters released their year ahead views in early calendar 2021, India stood alongside the US as the main source of upward revisions to world growth. March quarter data did nothing to challenge that.

Tragically, the story soon reversed 180 degrees. With a dramatic re–escalation of COVID–19 cases requiring strict restraints across many major economic and population centres, forecasts were marked down aggressively, even as the majority of emerging markets were seeing upward revisions to their growth trajectories.

The rebound observed in the wake of the June quarter lockdowns has once again seen activity rebound in decent fashion: and the way lockdowns were pursued in this latest round did significantly less damage to the overall economy than those of the prior year.

The key takeaway from all these rapid reversals is that India’s recovery trajectory and the associated release of pent–up demand will be spread somewhat more evenly across this calendar year and next than previously expected, rather than being heavily concentrated in calendar 2021.

Indian inflation has lifted sharply against this backdrop, with petroleum and food leading the way. The wholesale price index moved above 12% YoY in June 2021.

Beyond the immediate matter of COVID–19 recovery, returning India to a healthy and sustained medium–term growth trajectory will require a reduction in policy uncertainty, an increase in social stability, a greater focus on unlocking the country’s rich human potential, and an increase in international competitiveness in both manufacturing and traded services. The emphasis on moving up the “ease of doing business” rankings, and the steps taken to increase India’s share of geographically mobile foreign manufacturing investment that has come through during COVID–19 are both sensible steps.

Labour law reforms passed in 2019/20 are a significant positive for flexibility and simplicity, and should complement the focus on attracting foreign direct investors. The decision to be less engaged with the regional trade agreement landscape, and inconstant attitudes towards domestic market access for foreign players (be it old or new economy), collectively present a mixed message in terms of reform appetite, given the positive impact that freer trade and increased competition would have on productivity growth and innovation.

Briefly, we note that key economies in South-east Asia have been struggling with their latest waves of COVID–19. Collectively South-east Asia is not far behind India in scale (around 7½% of world GDP versus 8%), so this matters from a demand perspective. From a supply perspective, the region is also a globally significant supplier of a number of commodities, including natural rubber, palm oil, coal, copper, petroleum and nickel.

Steel and pig iron

Global crude steel production has begun to rebalance in calendar 2021, following two years of dramatic out–performance by China that occurred alongside depressingly weak outcomes in the rest of the world (ROW). Utilisation rates in the ROW are now back close to normal, on average, even as China continues to produce at spectacular run–rates. This produces a weighted global crude steel outcome for the first half of calendar 2021 of +17.9% YoY (+13.0% pig iron). That compares to –0.5% and –0.3% respectively in calendar 2020.

On current estimates, the world is expected to produce slightly more than 2 billion tonnes of crude steel in calendar 2021: needless to say, that is a record.

In calendar year 2019, Chinese production rose to 1.001 billion tonnes, exceeding the “mystical” nine zero level for the first time. After recording 1.065Bt of production in calendar 2020, China is on track to mildly exceed 1.1 Bt in calendar 2021, having already achieved a first half year-to-date run–rate of 1.14 Btpa (12% YoY), with April and May approaching a 1.2 Btpa pace. We expect an approximate 5% growth rate for production across the full calendar year 2021, noting that there are two obvious caveats to consider: (1) the degree of regulatory intervention, with the official intent to follow through on production cuts in the second half of this year recently re-affirmed, and (2) the possibility of further outbreaks of the delta variant of COVID–19, the control of which may have macroeconomic significance.

In the calendar year to date, we have seen broad–based strength across end–use sectors, with manufacturing (fuelled by strong exports and domestic machinery demand) faring somewhat better than construction, with growth in traditional infrastructure and housing starts softening in recent months.

China’s blast furnace (BF) utilisation rate has stayed at an elevated level, averaging above 90% in the first half of calendar 2021, approximately four percentage points higher than the same period last year. There has been significant volatility month–to–month due to both seasonal factors and localised regulatory intervention. Mills are cautious about how regulators will go about addressing their objective to contain steel output over the full year.

Pig iron has grown at a slower pace than crude steel in calendar 2021 to date, reflecting the aforementioned volatility in BF open rates as well as improved scrap availability for Chinese electric–arc furnace (EAF) mills, whose utilisation rates are up to 64% on average (18 percentage points higher YoY) with a peak above 80% in April. That said, EAF utilisation rates have fallen more recently as rebar margins have declined and power curbs have been instituted over the summer.

Finished steel inventories were a critical factor for market sentiment in calendar 2020, but they have taken a backseat to speculation about production cuts in calendar 2021 to date. The expectation of cuts has produced very strong implied ‘forward margins’ for steel mills, with steel futures anticipating price gains, but raw materials futures curves generally backwardated. This trend was at its starkest on the final trading day of July, when iron ore futures fell by –8% but steel futures moved moderately higher (1–3% depending upon the product). Realised margins have been highly volatile, with periods of break–even or loss–making and high profitability above $100/t observed within weeks of each other.

We note that net exports of steel-contained finished goods account for slightly less than 10% of Chinese apparent steel demand. That is a lower degree of external exposure than, say, Japan (22%) or Germany (21%). An additional 5% of Chinese production is exported directly. Low external exposure was seen to be a “good thing” in the dark early days of the pandemic: the reverse has turned out to be true as lockdowns have given way to a rapid rebound in the global trade in metal containing goods and in finished steel itself. Having seen their direct trade surplus in steel narrow and then turn to deficit in the middle of calendar 2020, Chinese mills came back quickly in calendar 2021, with the surplus rebuilt towards 52 Mtpa in H1 CY21. With an eye to their commitment to restrain growth in total steel production, the authorities stepped in at this point, cancelling export VAT rebates for most steel products and removed import tariffs for semi–finished steel. Gross exports are expected to halve – at least – in the remainder of the year.

Turning to the long term, we firmly believe that, by mid–century, China will almost double its accumulated stock of steel in use, which is currently 7–8 tonnes per capita, on its way to an urbanisation rate of around 80%13 and living standards around two–thirds of those in the United States. China’s current stock is well below the current US level of around 15 tonnes per capita. Germany, South Korea and Japan, which all share important points of commonality with China in terms of development strategy, economic geography and demography, have even higher stocks than the US.

We estimate that this stock will create a flow of potential end–of–life scrap sufficient to enable a doubling of China’s current scrap–to–steel ratio of around 20% by mid–century.14 As we argued in our blog on regional pathways for steel decarbonisation, increasing scrap availability is a powerful lever at the China industry’s disposal as it seeks to contribute to the national objective of net zero emissions by 2060. Beyond the considerable passive abatement opportunities available to it, of which scrap availability is the largest, the decarbonisation choices of Chinese steel mills will be determined by the age of their integrated steel making facilities, the policy framework they are presented with, developments in the external environment impacting upon Chinese competitiveness, and the rate at which transitional and alternative steel making technologies develop.

Steel production outside China (hereafter ROW) has recovered strongly from the mid–2020 collapse, with robust growth (albeit inflated by base effects) of 18 percent YoY in the first half of calendar 2021. To put that into more context, the year–to–date run–rate of 888 Mt is up modestly on calendar 2019 (882 Mt).

The combined ROW capacity utilisation rate had recovered most of the COVID–19 loss by the end of calendar 2020, and has been tracking close to normal ranges (72–75%) throughout the first half of calendar 2021.

In the calendar year to date, India’s crude steel output increased by +31.3% while pig iron output increased by +25.3% YoY. In the same period, output in Japan, Europe and South Korea increased by +13.8% (pig iron +10.4%), +18.3 percent (pig iron +14.3%) and +8.3% (pig iron +2.1%) YoY respectively.

Despite these superficially impressive growth rates in production, it has not been nearly enough to match the steep recovery in end–use demand. Inventory levels have fallen markedly and prices have accordingly surged – with some regions recording all–time records. As of July 2021, benchmark prices in India, Europe, and the US have surpassed US$1,000/t, US$1,400/t, and US$2,000/t respectively.

These record steel prices have produced impressively high margins – notwithstanding higher raw materials costs. ROW mills have predictably responded by seeking to raise productivity and secure the best quality raw materials, which has benefited branded medium and high grade iron ore products, direct charge materials like lump, as well as higher quality metallurgical coal. This major boost to profitability has provided a fillip to a number of struggling mills – it has been a tough few years for many ROW steel makers. The cash flow injection has also enabled an acceleration of deleveraging efforts and boosted shareholder returns. It may also be reflected in more ambitious decarbonisation efforts, the financing of which has always been a question mark in this traditionally low margin sector.

Despite the profitability sweet spot, protectionism remains a feature of the ROW industry landscape. The Biden administration has persisted with Section 232 tariffs, while the EU decided to extend their safeguard measures (which were due to expire in June 2021) by another three years. With tight supply driving steep inflation, demands from steel end–users has also prompted some countries to actively discourage exports. China’s efforts to curb steel exports were described above. Russia has imposed export tariffs (from August) to secure domestic supply and fight inflation – with other metals also included in the policy (such as nickel and copper). There is also speculation that Russia and the EU may be contemplating scrap export bans. China is somewhat unique in lowering barriers for the import of semi–finished steel, although at present there is very little incentive for ROW steelmakers to pursue sales into China given pricing in other regions is higher.

The release of the EU’s draft carbon border adjustment mechanism (CBAM) and the launch of China’s emissions trading system (ETS) are two important signposts for the steel industry decarbonisation. Note that steel is in the current scope for the proposed CBAM but not for phase one of the Chinese ETS, although it is expected to be included in the first expansion of the ETS’ scope, along with cement, when that occurs.

Iron ore

Iron ore prices (62%, CFR, Argus) have been very strong, ranging between $150/dmt and $236/dmt over the second half of financial year 2021, averaging around $183/dmt. The high for the period ($236/dmt, reached on May 12) is also the all–time record. Seaborne lump premia were elevated for much of the half, trading in the range of $0.21 to $0.77/dmtu (another all–time record, established on June 18), averaging $0.52/dmtu.

Six months ago, we provided the following précis of the state of play in the iron ore market:

“Iron ore prices have been elevated since the Brumadinho tailings dam tragedy in Brazil first disrupted the market in early 2019. Conditions were particularly tight in the recent half. The combined impact of very strong Chinese pig iron production and Brazilian exports being unable to lift materially from depressed calendar 2019 levels far out–weighted record shipments from Australia and strong output of Chinese domestic concentrate. Before prices can correct meaningfully from their current high levels, one or both of the Chinese demand/Brazilian supply factors will need to change materially.”

Fast forward to the end of the financial year, and neither of those nominated levers – Chinese demand nor Brazilian supply – had done anything to meaningfully disrupt the tight conditions in place at the time of our half year results. Brazilian exports have only managed to edge higher, while Chinese pig iron production has grown impressively again in calendar 2021 to date (4% YoY, a 920 Mtpa pace). In addition, new bullish demand factors for price have emerged, with ROW pig iron rebounding strongly and ex–China steel prices and margins ascending to spectacular levels. On the supply side, two of the major seaborne suppliers have delivered shipments at the lower end of their implied intra-year production guidance range as of June quarter reporting. With other sources of supply running essentially flat out already (record output from BHP and FMG, alongside elevated Chinese domestic and price sensitive seaborne) there was little opportunity for a bearish thesis on the market to sustain.

All of that said, the increasing likelihood of stern cuts to steel output in China in the current half year, as affirmed by China’s peak industry body in early August, is testing the bullish resolve of the futures markets. Prices have decreased materially in late July and early August, but they remain extremely high relative to history at around $160/t at the time of writing.

Chinese port stocks of all iron ore products15 closed the first half of the calendar year at 122 Mt, slightly lower than the closing position of 124 Mt in calendar year 2020. Unlike calendar 2020, there was not a great deal of volatility in aggregate stock levels in the first half of calendar 2021. Instead, sentiment was driven by the composition of those stocks. While overall fines stocks increased by +7 Mt over the half, premium branded fines16 declined by –8 Mt. Lump stocks were also run down over the half, to a two–year low of 17 Mt. These trends resulted in widening discounts for lower grade and unbranded products, higher realisations for medium and high grade branded products and very attractive premia for lump.

All–in–all, seaborne demand is expected to grow by around 5% in calendar 2021 against just 1% growth in supply from the seaborne majors. ROW has provided strong support on the demand side in calendar 2021, in contract to calendar 2020. Once again, the caveat is the depth and timing of mandated cuts to steel production in China.

We estimate that price sensitive seaborne supply will increase by around +22 Mt (natural grade wet basis) in calendar 2021, on top of growth of around +40 Mt in calendar 2020. Given prices have been elevated for a considerable time now, it seems unlikely that there is any supply in this category that has been withheld for discretionary reasons in the cycle to date. That means any further increases in the near term are likely to be hard won through productivity gains.

Chinese domestic iron ore concentrate production has increased in each of the last three years. Output reached 247 Mt in calendar year 2020, with additional growth of 15–25 Mt expected across calendar years 2021 and 2022 combined. The peak run–rate in this phase has been 264 Mtpa: about 10 Mt higher than levels reached under “surge” conditions in previous periods of attractive prices.17 Going forward, we expect that, in addition to structural market based drivers, safety and environmental inspections are likely to have a material influence on the average level and seasonal volatility of Chinese domestic iron ore production.

On the topic of differentials, calendar 2021 to date has been much more favourable to direct charge materials than was calendar 2020. Recall that premia for direct–charge materials compressed heavily for much of calendar 2020, with strong lump supply out of Australia and redirected pellet cargoes from Europe contributing to a build–up in port stocks of these products even as fines inventories were declining to multi–year lows. These unique circumstances have since reversed decisively, with lump premia specifically spiking substantially higher in June 2021 to $0.77 per dmtu, up from a meagre $0.04/dmtu during the rainy season lull in mid–2020. Half–on–half, the lump premia has increased by 127%. On the demand side, lump benefited from extended sintering restrictions in northern China and a productivity push in ROW under very attractive margin conditions.

Fines differentials to the 62% index for the 65% and 58% indexes widened considerably half–on–half following the improved average steel margin (higher premiums for higher grade, larger discounts for lower grade).

In the medium to long–term, as described in our steel decarbonisation blogs (episodes 2 and 3 in our Pathways to Decarbonisation series) high quality iron ore fines and direct charge materials such as lump are important abatement sources for the blast–furnace steel making route during the optimisation phase of our three–stage Steel Decarbonisation Framework. In China of course, the BF–BOF route represents roughly 90% of steel–making capacity, with the average integrated facility being just 10–12 years old. BHP’s South Flank project, which achieved first production in May 2021, will raise the average iron ore grade of our overall portfolio by around 1%, in addition to increasing the share of lump in our total output from around one–quarter to around one–third.

Our analysis indicates that the long run price will likely be set by a higher–cost, lower value–in–use asset in either Australia or Brazil. That assessment is robust to the prospective entry of new supply from West Africa, the likelihood of which has increased. This implies that it will be even more important to create competitive advantage and to grow value through driving exceptional operational performance.

Metallurgical coal

Metallurgical coal prices18 have been extremely volatile. In the half year just concluded, the PLV index ranged from a low of $102/t FOB Australia to a high of around $194/t. MV64 has ranged from $94/t to around $168/t; PCI has ranged from $92/t to $145/t; and SSCC has ranged from $85/t to $137/t. Three–fifths of our tonnes reference the PLV FOB index, approximately.

For the half year overall, the PLV index averaged $132/t, up by 18% compared to the prior half but down by –3% YoY. The differential between the PLV and MV64 indexes averaged 9% in the second half of financial year 2021, 8 percentage points lower than in the previous half. Those figures hide considerable change within the half. The spread narrowed to 5% in April before widening to 14% in June.

As the foregoing summary attests, prices faced by Australian metallurgical coal producers in the free–on–board (FOB) market were weak for most of the 2021 financial year. Chinese import policies have been a major driver in price formation and market development since October 2020, when it ceased to serve as the effective clearing market for all seaborne coal. China’s import policy towards Australian coals has impacted natural trade–flows, driven domestic prices for end–users in China higher and created two distinct trading markets: the traditional FOB market for ex-China [ROW] regions (potentially serviced by all seaborne producers, but the only market for Australian products) and the China CFR market, serviced only by non–Australian producers. From its inception, this “tale of two markets” was, and is, the dominant story in the metallurgical coal trade.

To understand the profound impact of the distortions, a bit of history is required. Australia was responsible for between 57% and 61% of total seaborne exports of metallurgical coal by volume from 2017 to 2020. The next largest supplier in that period, the US, averaged just 16% of exports. On the demand side, there is more diversity, with China, Japan, the EU and India all taking roughly one–fifth of seaborne imports, with South Korea an important fifth player. Unsurprisingly, given Australia’s large role in the export side of the trade, and its proximity to North Asia, Australia was China’s number one seaborne coking coal import supplier in each of those years, with shipments averaging around 40 Mtpa.19

Despite the introduction of flexibly applied annual import quotas for total coal imports (i.e. energy and metallurgical) in China from calendar 2017 forwards, a policy that initially sought to defend the financial sustainability gains that China’s enormous domestic coal industry had made under Supply Side Reform, China’s overall import needs (in addition to its dynamic trader network and impressive infrastructure for housing the bulk commodity trade), made it a highly effective “clearing market” for the global metallurgical coal trade. This status was never more evident than during the peak of COVID–19 induced lockdowns in the ROW in the June quarter of 2020.

As is generally the case where a clearing market is operating effectively and trade outcomes are the result of private actors optimising commercially, the scale of the netback differential between the Chinese PLV CFR index and the PLV FOB Australia index was kept in check by arbitrage in the physical trade.20

To recap, Australia was both the largest seaborne exporter of metallurgical coal and the largest seaborne supplier to the clearing market, China. Therefore, this bilateral trading relationship was much more than just one of many in a vibrant and competitive global trade – it was the sun around which the other planets of the met coal solar system orbited.

All this changed abruptly in the last few months of calendar 2020:

- Trade volumes from Australia to China dropped to zero. Australian coal producers obviously had to find alternative destinations for all of the product normally earmarked for China extremely quickly, with all of the disadvantages that entailed. Chinese buyers of Australian coal had to find alternative supply sources equally fast.

- The predictable impact of the scramble to disrupt the regular flow of trade was that FOB Australia prices went down (sellers luring new buyers) and China CFR prices went up (buyers luring new sellers). This saw the freight adjusted spread between FOB Australia and China CFR widen dramatically to an average of over $85/t.

- This spike in the differential tempted some non–Australian seaborne coals naturally predestined for other markets (for example US into Europe) to be redirected to China.

These market dynamics are discussed in more detail below.

As hard import curbs on Australian origin coals into China were instituted, bilateral trade volume fell to zero and FOB prices wallowed around $100/t (below the 75th percentile of the cash operating cost curve). Vessel queues of Australian coals waiting off the Chinese coast spiked to around 46 at the end of December 2020 (roughly 5 Mt of floating metallurgical coal) while the Chinese owners of these cargoes unsuccessfully attempted to get them discharged and cleared through customs. At the same time, with demand for metallurgical coal buoyed by very strong growth in pig iron production, domestic PLV prices in China surged to well over $200/t, dragging up the seaborne CFR price by over $50 in late calendar year 2020. This was the point at which PLV FOB Australia and the China CFR index first diverged dramatically. (A Capesize vessel could be piloted through the gap between them at the time of writing.)

North American coal producers, who have typically shipped less than 10% of their volumes to China, were now enjoying a premium of $50–100/t for shipments to China versus sales into their traditional markets. The result was a swift reshuffle in trade flows, with the Atlantic trade subordinated in favour of the Pacific. By the first half of calendar 2021, China’s share of North American coal exports had increased by 15 percentage points to around 25%.

As indicated above, Australian metallurgical coal shipments to China have averaged 40 Mt over the last five years, making up slightly over one–fifth of overall Australian exports. The remaining volume sold to ROW is split between Developed Asia (36%), India (24%), Europe (9%), South-east Asia (4%) and Brazil (plus other, 4%). Whilst Australian producers are unable to access China, they are obviously impelled to redirect all volumes to ROW. In addition to extremely nimble commerciality, three factors have been working to mitigate the physical disruption and value-leakage caused by this non-discretionary redirection of trade flows.

- Constrained Supply: Australian shipments were adversely impacted by safety concerns at some mines in Queensland, weather and some production curtailment decisions as prices moved deep into the cost curve. While exports were flat YoY in the calendar year–to–May (noting calendar 2020 volume was at a seven year low), versus the five-year average they are down –1.8%. Versus calendar 2019 they are –4.8% lower.

- Demand recovery in ROW and strong operating conditions for the steel industry. Blast furnace operating rates have normalised across ROW as a whole. Despite a devastating second wave of COVID–19 infections, India’s metallurgical coal imports increased by +33% YoY, annualised calendar year–to–May. Europe and Developed Asia witnessed +11% and +6.9% YoY growth in pig iron production on the same basis. Australia’s export share to these regions increased to around 90%: Developed Asia (42%); India (35%); and Europe (10%).

- Increasing trade redirection from North America to China (as described above) created a supply shortfall in the Atlantic at a time of record steel prices and margins. This was catered to by Australian suppliers. This “rebalancing” lifted PLV FOB Australia out of the trough seen earlier in this calendar year.

Notwithstanding the ongoing distortions in the metallurgical coal market, PLV FOB Australia rallied significantly late in financial year 2021. The immediate catalyst was disrupted supply in China itself (safety concerns leading to widespread mine suspensions) and its landborne trade partner, Mongolia (COVID-19 border closures).

Looking at the Chinese and Mongolian disruptions in a little more detail, the COVID–19 situation in Mongolia deteriorated starkly from early May 2021. This resulted in the closure of the two main truck border crossings with China. Coking coal truck flow was roughly 720 trucks per day in calendar 2019 – the year when Mongolia was China’s largest source of imports. That slowed to a mere trickle in June 2021, with only moderate recovery in July. Separately, a series of fatal mining accidents in China jolted the government’s objective of “sustainable mining”, forcing the suspension of a significant proportion of higher quality coking coal capacity.

Chinese domestic PLV prices surged to record levels well above $300/t as local fundamentals tightened quickly (and the price has since ascended to around $440/t at the time of writing). This set off an immediate chain reaction in the seaborne trade, similar to the slower moving trends seen earlier in the year, but compressed into weeks. These events highlight that even though Australian exporters and Chinese importers are not transacting bilaterally at present, the China CFR and Australian FOB markets are still directly influenced by each other via the overlap of ex-China demand and ex-Australian supply.

Going forward, despite the recent exuberance, while natural trade flows are inhibited the met coal industry faces a difficult and uncertain period ahead.

Longer term, we argue that the continued policy focus on environmental considerations and financial sustainability in Chinese coal mining, in addition to the intent to embark upon a decarbonisation path for steel making, should highlight the competitive value of using high quality Australian coals in China’s world class fleet of coastal integrated mills. As we argued here, China’s steel industry is still in the optimisation phase of its decarbonisation journey, in which higher quality raw materials make a clear difference to the energy and emissions intensity of the BF–BOF21 route, which accounts for 90% of Chinese and 70% of global crude steel production.

In coming years, most committed and prospective new metallurgical coal supply is expected to be mid quality or lower, while industry intelligence implies that some mature assets are drifting down the quality spectrum as they age.

The relative supply equation underscores that a durable scarcity premium for true PLV coals is a reasonable starting point for considering medium terms trends in the industry. The advantages of the highest quality coking coals with respect to emissions are an additional factor supporting this overarching industry theme: an advantage that will be increasingly apparent as carbon pricing becomes more pervasive.

The flip side of PLV “privilege”, as derived from the fundamentals discussed above, is that the non–PLV pool could face fundamental headwinds for an extended period in the disrupted post COVID–19 world.

On the topic of technological disruption, our analysis suggests that blast furnace (BF) iron making, which depends on coke made from metallurgical coal, is unlikely to be displaced at scale by emergent technologies this half century. The argument hinges partly on the sheer scale of the existing stock of long–lived BF–BOF capacity (70% of global capacity today, average fleet age22 of just 10–12 years in China and around 18 years in India). It also highlights the lack of cost competitiveness, technological readiness (or both) that is expected to inhibit a wide adoption of potentially promising alternative iron and steel making routes, or high–cost abatement levers such as hydrogen iron making and carbon capture and storage, for a couple of decades at least. Notwithstanding the current sweet spot in profitability under record pricing in many regions, steelmaking is a low margin industry where every cent on the cost line counts.

We certainly acknowledge that (a) PCI could be partially displaced in the BF at some point by a lower carbon fuel, and (b) the well–established electric arc furnace (EAF) technology, charged with scrap and without any need for metallurgical coal, will be a stern competitor for the BF at scale to the extent that local scrap availability allows. In a decarbonising world, EAFs with reliable scrap supply running on renewable power should be very competitive. We assess that emerging technologies that are expected to feature in a low carbon end-state for the industry, such as green hydrogen enabled DRI-EAF, to be some decades away from being deployed at scale. Accordingly, we expect that the industry will need to be a purchaser of carbon offsets (as required to meet regulatory or voluntary commitments) for a considerable period of time even as it positions itself to pursue long run carbon neutrality.

Information on our Scope 3 partnerships with China Baowu, HBIS and Japan’s JFE Steel is available on our website.

Copper

Copper prices ranged from $7,756/t to $10,725/t ($3.52/lb to $4.86/lb) over the second half of the 2021 financial year, averaging $9,092/t ($4.12/lb). The average was around +33% higher than in the prior half and +65% versus the equivalent half of financial year 2020.23 The average for the full financial year 2021 was $7,944/t.

Both industry specific fundamental factors and swings in broader macro sentiment have been influential factors in price formation over the last 12 months. Bullish investor sentiment crested in late April, early May 2021, with the LME establishing a new all-time official cash high of $10,725/t on May 10, with 3-month intra-day pricing peaking at $10,747.5/t. Prices have receded a little since that time, trading above $9000/t but below $10,000/t in the second half of June and through July and early August. That, of course, is still very elevated relative to both history and the position of the operating cost curve.

The size of the wedge that opened up between copper demand in China (roughly half of refined demand) and the ROW in calendar 2020 has narrowed over the last half year. Chinese semis demand was up by 0.7% in calendar 2020, while ex–China markets declined by around –9%, for a global figure of –4.5%. As of June 2021, we expect growth for the full calendar year to come in at around 6% and 9% for China and ROW respectively, with global demand around 7½%. The volume of world demand in calendar 2021 is expected to surpass 2019 levels by around 2¾%.

Turning to Chinese demand first of all, on an end–use basis the performance was mixed by sector in calendar 2020, and overall growth trailed well behind steel (0.7% versus around 6% for steel). Demand conditions have firmed and broadened noticeably in the first half of calendar 2021 though, as expected.

White goods, transportation, machinery and electronics have all enjoyed good momentum in the first half, with export sales a considerable support. Where white goods are concerned, customer intelligence indicates that this is more of a volume boost than a genuine profit boom for downstream manufacturers, as rising input costs are difficult to pass on in this highly competitive, price-sensitive market.

Construction has posted modest growth in the calendar year-to-date. However, with a housing completion upcycle underway even as new starts flatten out (see further discussion under the Chinese economy above), copper demand growth from real estate is likely to out-perform the leading and coincident indicators for the sector (e.g. housing sales and under-construction) for some time to come.

Infrastructure (comprising both grid spending and power generation projects) has slowed down a little in recent months. Anecdotally, high prices may have led to some project delays, with State Grid reportedly working within a relatively steady nominal budget for the calendar year. Power generation investment though continues to expand. Low carbon technologies are an increasingly important element of this component of demand, with China’s boom in offshore wind capacity in particular a boon for copper. Wind’s share of power source investment in China has doubled to around 50% between calendar 2018 and 2020.

Demand from the ROW has recovered strongly from its steep contraction in calendar 2020, with high single-digit growth anticipated for calendar 2021 as a whole. Developed regions are leading the way, with volumes in the US and Europe moving back above the calendar 2019 level over this course of this year. The major regions of the developing world (and Developed Asia) are lagging moderately behind the North Atlantic recovery. They are accordingly not expected to reach that key milestone until calendar 2022.

On the supply side of the industry, the copper concentrate balance has remained tight, with treatment and refining charges (TCRCs) moving down (i.e. in the producers’ favour), towards decade lows.24 The FastMarkets spot TC index fell to just 21.9 on April 9, although it had rebounded somewhat as the financial year closed. While the localised risks from COVID-19 and other forms of potential disruption (for example community protests or labour negotiations) remain elevated, industry-wide operational performance was sound in the first half of the calendar year. As of July 30, 2021 (i.e. with the benefit of some but not all June quarter operational reviews), Wood Mackenzie had identified 420kt of disrupted production year–to–date, or 1.9% of initial production expectations. That compares to 4.0% at the same point of calendar 2020 and 2.2% at the same point of calendar 2019.

Scrap availability was constrained globally, for policy, logistical and economic reasons across calendar 2019 and 2020. However, scrap is rebounding solidly in calendar 2021 and we expect scrap use to grind upwards as a structural trend in the 2020s due to both supply and demand drivers.

Turning to the outlook, the next cyclical challenge for the market is expected to come when a cluster of in–development projects (including in Peru, Chile, central Africa and Mongolia) come on–stream somewhere in the 2022–2024 window, even as the scrap share of copper units moves higher. The scrap uptrend is supported by the increasing size of the end–of–life pool in China, high prices and fewer physical constraints from social distancing. Once that phase of the decade is navigated, a structural deficit is expected to open in the mid–to–late 2020s, at which point we again see some sustained upside for prices.

A “take–off” of demand from copper–intensive easier–to–abate sectors (renewable power generation, the electrification of light duty transport, and the infrastructure that supports them both) is expected to be a key feature of industry dynamics in the second half of the 2020s: if not earlier.

Looking even further out, long term demand from traditional end–uses is expected to be solid, while broad exposure to the electrification mega–trend offers attractive upside. Grade decline, resource depletion, water constraints, the increased depth and complexity of known development options and a scarcity of high–quality future development opportunities are likely to result in the higher prices needed to attract sufficient investment to balance the market.

On this latter point, it is notable that there has not been a material uplift in project announcements this year, despite the very strong price backdrop and copper’s future-facing halo effect. That underscores the idea that the option set of the industry as a whole is constrained. It may also reflect policy and political uncertainty, with both Chile and Peru (together about two-fifths of world mine supply) presenting a fluid regulatory picture to would-be investors.

It is these multiple parameters that are critical for assessing where the marginal tonne of primary copper will come from in the long run and what it will cost. Working off a 2019 operating asset baseline, we estimate that grade decline could remove approximately –2 Mt per annum of mine supply by 2030, with resource depletion potentially removing an additional –1½ and –2¼ Mt per annum by this date, depending upon the specifics of the case under consideration. Note that resource depletion depends in part on decisions to close or extend the life of aged assets, which in turn will depend upon, among other things, price expectations and the regulatory environment.

Our view is that the price setting marginal tonne a decade hence will come from either a lower grade brownfield expansion in a lower risk jurisdiction, or a higher grade greenfield in a higher risk jurisdiction. Neither source of metal is likely to come cheaply.

Crude oil

Crude oil prices (Brent) ranged from a low of around $51/bbl to a high of around $76/bbl in the second half of financial year 2021. Brent was up by around 47% from the average of the prior half. West Texas Intermediate (WTI) Cushing ranged from $48/bbl to $74/bbl.

The front–month Brent minus WTI spread widened on average half–on–half, expanding modestly to $3.12/bbl in the second half of the financial year 2021 from $2.35/bbl in the first. The WTI minus MARS25 spread has averaged around –$0.58/bbl for the last twelve months (i.e. MARS at a premium to WTI), but just $0.25/bbl in the most recent half.

Six months ago we stated that “While we are confident that demand will rebound elastically this calendar year, and the price path will have an upward tilt on average, the situation remains complex. The tapering of OPEC+ cuts, the possibility of lower cost US shale assets hedging their way back in … are … likely to lean against the price recovery.” As it happens, neither of those key macro supply risks eventuated. Indeed, both OPEC+ and US shale have been even more disciplined than we thought was likely once prices sustained above $60/bbl WTI. The fact discipline has been steadfastly maintained in US shale with WTI spending a number of months around $70/bbl is telling.

Prices evolved in three stages over the first half of calendar 2021. The first stage lasted from January to mid-March. A sequence of price-positive demand and supply surprises relative to expectations saw Brent lift from just below $50 at the beginning of the period to around $66/bbl on March 11. The recovery in mobility across the world and the aggressive stimulus intentions of the US Biden administration were two major drivers of demand expectations. On the supply side, Saudi Arabia (KSA) led OPEC+ in a disciplined direction, partly via self-sacrifice, which calmed market nerves about an excessively rapid return of curtailed supply.

The second stage ran from mid-March to late-May: a relatively narrow range trade centred on the low-to-mid $60/bbl region. The third stage runs from late May up to the time of writing in early August. Prices have added a further $10/bbl or so over this period. Alongside mounting evidence that inventories were drawing down globally, the key sources of volatility in this phase were geopolitical: US-Iran relations and OPEC+ group dynamics. The possibility of a new US-Iran nuclear pact, allowing for the lifting of sanctions on Iranian crude exports, was a major story in June in the weeks leading up to Iran’s Presidential election (June 21st). The lifting of sanctions would lead to roughly 2 Mbpd of additional supply entering world markets (noting Iran consumes around 2 Mbpd domestically). President-elect Raisi immediately watered down that speculation, adopting a hawkish tone on foreign policy in the lead up to his inauguration on August 3.

Moving onto OPEC+, there was considerable nervousness whether the UAE’s desire to reset their quota baseline would not only delay an OPEC+ deal being done in early July: it might be a preliminary to a wider split within the group and a disorderly rebound in supply. These fears proved unfounded. On July 18 OPEC+ announced a benign deal that was greeted with relief. New baselines were negotiated for five members, including UAE, kicking in from May-2022. And a steady approach to returning the group’s remaining 5.8 Mbpd of curtailed barrels into circulation was outlined: a stable pace of 0.4 Mbpd per month to April-2022 and 0.43 Mbpd per month from May-2022 to September-2022.

We are just as cognizant of potential short-term upside risks on demand as we were six months ago.

Under ordinary circumstances, 1 percentage point of growth in world GDP tends to be associated with 0.3–0.5 percentage points of oil demand growth. In other words, oil demand is a relatively stable function of overall economic activity and it is also typically less volatile than the broader economy. However, oil demand fell by much more than GDP in 2020 due to the unique circumstances of the Great Lockdown. For the calendar year as a whole, world GDP contracted by –3.2% and oil demand by –8.5%: or a ratio of –2.7 to –1. That is a 9 fold increase in sensitivity. With world GDP flipping to well above trend growth in both calendar 2021 and calendar 2022, if the sensitivity stays high (say, greater than 1) then oil demand could move very rapidly indeed.

Shifting to the longer term, while demand was hit very hard in the short–term, it is still uncertain to what degree, if any, demand has been impaired structurally. We have previously outlined our preliminary analysis on potential headwinds coming from (1) the loss of vehicle miles from less commuter travel (2) reduced aviation intensity (3) policy support for EVs accelerating take-up beyond our already aggressive assumptions (4) Weaker economic growth in the populous developing countries hardest hit by COVID–19, leading to slower uptake of auto ownership and slower growth in demand for logistics and air travel, was a further possibility. Tailwinds from an increased desire for auto ownership, as a result of a decreased desire to use public transport, have also emerged. In the US for example, where auto ownership might reasonably have been seen to have reached saturation levels, both new and used car sales turnover have spiked higher.26

The supply side of the oil industry slashed capital spending plans in the face of the conditions that calendar 2020 presented. According to consultancy Rystad, final investment decisions (FIDs) for greenfield projects fell back to 1950s levels. The IEA has estimated that upstream petroleum capex declined by –31% in calendar 202027 and a similar scale of decline in downstream and infrastructure. Interestingly, in the last big capex crunch (calendar 2016), upstream fell by around a quarter: but the rest of the value chain was resilient, lifting 4% in the same year.

The IEA forecasts that total upstream investment will come back a modest 8% in calendar 2021. Within that, IOCs are expected to see spending flat to down overall, with much of the growth coming from NOCs, led by China and the Middle East, with Saudi Aramco, Abu Dhabi National Oil Company and PetroChina all in upstream expansion mode.

If the IEA forecast were to eventuate, total upstream spending in calendar 2021 would be 44% below the level of 2015, but with a higher price backdrop.

In a sector subject to the perpetual tyranny of field decline, with (conservatively) a third of on–stream barrels needing to be replaced on a rolling ten–year cycle, that is also coming off a relatively unsuccessful decade for exploration, an investment and exploration crunch of this magnitude is expected to have major ramifications for supply for some time to come. The markedly higher levels of upstream activity from NOCs versus the IOCs as the industry embarks in earnest on the energy transition era, also imply that the current imbalance between sovereign and non-sovereign controlled oil reserves (the former control around two-thirds of the total28) will only get wider in coming years.

Our base case is that demand will rise modestly above pre–COVID levels in the coming years, before reaching a plateau in the medium run. In the phase that precedes the plateau, the twin disruptive levers of efficiency and electrification that are operating on the road transport segment are more than offset, from a total liquids demand perspective, by the impact of rising living standards in the developing world.

But these circumstances are not expected to last forever. Beyond the plateau, we foresee a steady erosion of demand as the disruptive forces gain ascendancy over the traditional economic development drivers, assisted by policy changes and, most importantly, technological progress. The ability of developing countries to leapfrog in their technology choices as cost relativities evolve (subject to infrastructure availability) is expected to ensure that their future pathways of oil use per head track somewhat lower than the historical pathways pursued by the major OECD economies.

Future patterns of urban infrastructure design and country specific population density and agglomeration characteristics also play a role in this assessment.29

Bringing this bottom–up analysis of demand together with systematic decline rates of around 3% per annum (global weighted average) that the supply side of the industry is subject to, points to an expected structural supply-demand gap through at least the mid–2030s. This analysis indicates that considerable investment in conventional oil is going to be required to fill that gap and maintain market balance. If that investment is not forthcoming in a timely way, the possibility of oil prices flying-up aggressively cannot be ruled out.

Liquified natural gas (LNG)

The Japan–Korea Marker (JKM) price for LNG has been extraordinarily volatile over the last eighteen months. Spot prices hit record lows as COVID–19 demand destruction hit a market already facing excess supply and large storage builds in the first half of calendar 2020. The market then reversed course sharply during the northern winter, printing record high prices in January 2021. And then, prices performed stronger through shoulder season, and moved higher again going into the northern hemisphere summer.

The average price for the half year just concluded was $9.99/MMbtu, +72% higher than the prior half, with the full financial year 2021 averaging $7.88/MMbtu, +94% higher than financial year 2020.

The fundamental starting point for financial year 2022 features a relatively lean storage position and constrained supply that is stretched to service robust demand coming from power and non–power sources in both East Asia and Europe. High carbon allowance pricing in Europe, and elevated energy coal prices, are both LNG positive, all else equal.

Looking further ahead, within our generally constructive outlook for LNG demand growth, the key uncertainties include energy mix and decarbonisation policies in Japan, China and Korea in the wake of their net zero pledges. At the national level, the scale of competing supply of indigenous and pipeline gas in (and into) China30; the level of investment in new gas infrastructure in India; and the timing and scale of nuclear restarts in Japan are also potential swing factors in the outlook. Outside Asia, the amount of Russian pipeline gas supplied to Europe, plus energy mix and decarbonisation policies in the EU are all material sources of uncertainty.

Despite the healthy LNG demand growth that we project, and even with only a single project reaching final–investment–decision (FID) in calendar 2020, and three more in calendar 2021 to date, such was the flurry of FID activity in 2019 that we felt current and committed capacity was likely to amply supply the market until the middle of this decade. However, with a question mark now hanging over the future of developments in Mozambique, where dangerous levels of unrest in the province of Cabo Delgado have forced projects to go on hold and FIDs to be deferred, that may no longer be the case: notwithstanding Qatar’s substantial expansion plans (as officially sanctioned in February 2021).

Beyond the mid–2020s, new projects are expected to be required in a global gas market where the marginal supply looks likely to come from North American LNG exports under a range of scenarios.

In the longer term, we see LNG as a commodity that has an opportunity to operate under inducement economics, at times, given the combination of systematic base decline and an attractive demand trajectory. Global gas is also a big market that is getting bigger, with LNG expected to almost double its share of that expanding pie. However, gas resource is abundant and liquefaction infrastructure comes with large upfront costs and extended pay backs. There is though considerable heterogeneity in terms of the full lifecycle carbon-equivalent footprint of different resources. The answer to this complicated equation is that, in our view, only assets that are advantaged by proximity to existing infrastructure, or customers, or both, with competitive carbon intensity, are fundamentally attractive.

Eastern Australian gas

The rise of Queensland coal–bed methane resources and the maturation of conventional fields in Bass Strait and the Cooper Basin have combined to alter the fundamentals of domestic gas supply to Eastern Australia (EA). The announced expansion of the South West Queensland Pipeline validates this shifting supply dynamic. Our assessment remains that the EA market is likely to ultimately harmonise around LNG netback pricing. While progress on LNG import project(s) has been observed to slow, we expect that this supply source is likely to be required to meet peak seasonal demand in the future. We expect that this development would accelerate the LNG netback harmonisation process, as well as improving the transparency of domestic price discovery.