BHP's economic and commodity outlook (FY20 half year)

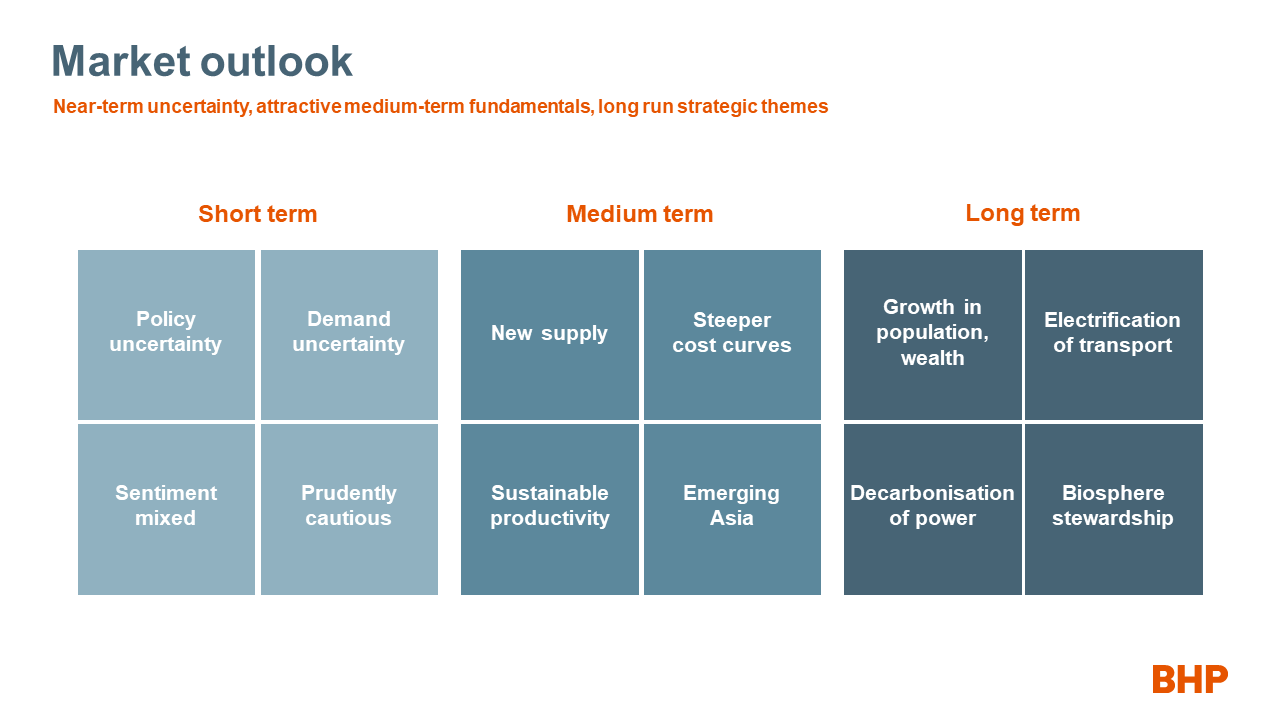

Six months ago, at the time of our full year results for the 2019 financial year, an air of prudent caution permeated commodity markets. On balance, events since that time have justified that caution.

The result has been a mixed price performance by our key commodities.1

Demand for oil, metallurgical coal and copper was weaker than expected in the 2019 calendar year, while demand for iron ore was higher than expectations. These outcomes reflected the impact of stunted growth in international trade, a recession in the global auto sector, a broad based slowdown in manufacturing in the developed world and a challenging year for non–China emerging markets, including India. The negative factors were partially balanced by robust growth in Chinese steel production and resilient growth in the United States for the majority of the calendar year.

On balance, we expect to see lower iron ore prices on average in calendar year 2020 than in the year just concluded, with considerable two–way volatility in prospect. On the other hand, we expect conditions in metallurgical coal to improve somewhat versus those experienced in the second half of calendar 2019. Product differentials in both commodities are expected to remain favourable for higher quality producers, albeit narrower than the extremes of recent history, as steel industry profitability normalises.

Oil and copper prices are highly susceptible to swings in global policy and economic uncertainty. We consider the underlying commodity–specific fundamentals of both the oil and copper markets to be sound. We estimate that their forward looking short–term fair value ranges are similar to those we estimated both six and 12 months ago. Now that the US–China “Phase One” trade deal has been signed, a major drag on sentiment for much of calendar year 2019 has been neutralised. While this remains the case, we have no particular bias within those ranges.

The caveat is that while we hope that the Covid–19 outbreak is speedily contained within the March quarter, no one can be adamant about the precise timing. While the world is forced to live with this unknown, there is likely to be a sentiment discount in the prices of these commodities.

Looking beyond the immediate picture to the medium–term, we see the need for additional supply, both new and replacement, to be induced across most of the sectors in which we operate.

In many cases, this could lead to higher–cost supply entering the cost curve.

This projected steepening of cost curves can reasonably be expected to reward disciplined owner–operators with high quality assets.

On the demand side, we continue to see emerging Asia as an opportunity rich region. China, India, ASEAN and the global impact of China’s Belt and Road initiative are all expected to provide additional demand for our products.

As the true economic costs of trade protection are progressively recognised by global consumers, we anticipate a popular mandate for a more open international trading environment will eventually emerge.

Looking even further ahead, the basic elements of our positive long–term view remain in place.

Population growth and rising living standards are likely to drive demand for energy, metals, and fertilisers for decades to come.

New demand centres will emerge where the twin levers of industrialisation and urbanisation are still developing today. The electrification of transport and the decarbonisation of stationary power will progress. Comprehensive stewardship of the biosphere and ethical end–to–end supply chains will become even more important for earning and retaining community and investor trust.

The ability to both provide and demonstrate social value to our host communities and in our customer jurisdictions will be a core enabler of our strategy and a source of competitive advantage.

Against that backdrop, we are confident we have the right assets in the right commodities in the right jurisdictions, with attractive optionality, with demand diversified by end–use sector and geography, allied to the right social value proposition.

Even so, we remain alert to opportunities to expand our suite of options in attractive commodities that will perform well in the world we face today, and will remain resilient to, or prosper in, the uncertain world we will face tomorrow.

Table of contents

| World GDP > | China > |

| Major advanced > | India > |

| Steel > | Iron ore > |

| Met coal > | Copper > |

| Crude oil > | LNG > |

| Eastern Aust gas > | Aust power > |

| Energy coal > | Potash > |

| Nickel > | Freight > |

| Inflation > | EVs > |