$name

The first episode in our decarbonisation series looked at the critical enabler of achieving zero-carbon power generation. The second introduced our framework for assessing steel decarbonisation prospects, alongside a discussion of the current and emerging abatement levers the industry may deploy. This episode builds on that analysis to consider the most likely regional decarbonisation pathways. With China, Japan and South Korea all announcing national net zero ambitions in recent times, and Europe accelerating their longer-held ambitions, a regional narrative is particularly timely.

Our major conclusions are that:

- Decarbonisation pathways will reflect regional realities, and given very diverse starting points, the pathways are unlikely to converge on a single model for many decades.

- Aggressive policy and rapid advancement in general-purpose decarbonisation technologies are clearly required to induce higher-impact, higher-cost abatement levers across all regions.

- Notwithstanding the welcome uplift in regional decarbonisation ambitions we have seen of late, ‘hard-to-abate’ steel sectors in most regions face challenges to reach the green end state by 2050.

- An immense challenge awaits in developing regions such as India and Southeast Asia, where demand growth seems likely to heavily outweigh major prospective gains in efficiency.

Strong growth in steel demand in recent decades has seen absolute emissions from the sector increase, notwithstanding considerable achievements in the environmental profile of the global fleet and impressive gains in energy efficiency and carbon intensity (CO2 per tonne steel) dating back to the 1990s. First, the collapse of the Soviet Union saw a step change in steel emissions from the region. Second, the obsolete open-hearth furnace (OHF) has been largely phased out worldwide. Third, the modernisation of the Chinese steel industry - with new, state-of-the-art capacity and relentless environmental campaigns - has lowered the energy intensity per tonne of steel by more than 60% since 1990. Fourth, rising scrap availability in the developed world has also enabled a reduction in the carbon intensity of steelmaking in regions like the US and EU. And fifth, in Japan and South Korea, considerable technical efforts and increasing scale have moved the efficiency frontier of the blast furnace outwards.

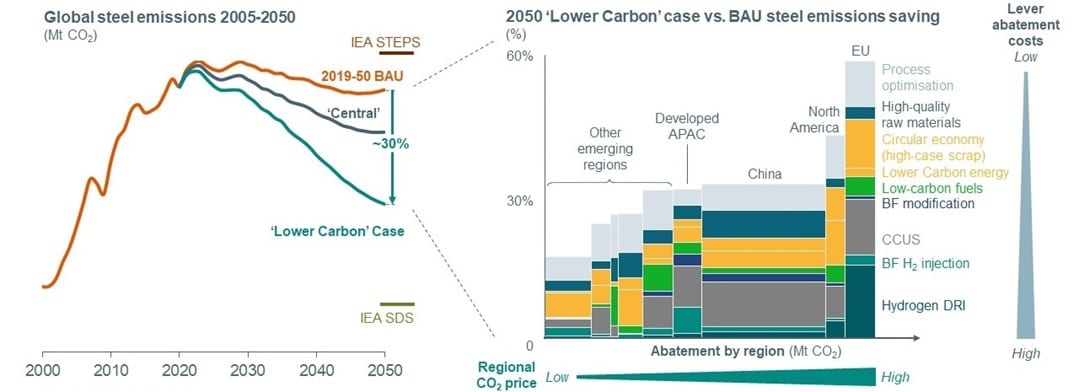

In a ‘business as usual’ (BAU) case , where demand growth is offset solely by ‘passive abatement’ opportunities that are available due to growing scrap supply and positive changes in the power mix, the global steel emissions baseline (absolute levels) will decline only marginally by 2050. While the emissions intensity per unit of steel will decrease noticeably, the industry would still fall far short of any desirable decarbonisation targets. This underscores the magnitude of the challenge that stands before the industry. Incrementalism will not win the day.

Figure 1 Global historical steel emissions and BAU case analysis in 2019-2050 (Mtpa CO2)

Sources: BHP analysis; worldsteel

Note:

- Steel output increase multiplying with initial base year emissions intensity.

- Include technological shifts, efficiency gains and passive abatement levers such as steel metallic and power mix changes from 1990 to 2019.

- Central-case scrap availability increase and business-as-usual natural-gas DRI development in gas-rich traditional markets.

Our steel decarbonisation framework highlights three distinct stages, beginning with the optimisation of existing technology and concluding with the green end state. Different types of abatement levers are adopted in each stage, with each region’s starting point in terms of indigenous fleet, infrastructure and feedstock availability a major influence on when these levers are likely to be pulled at scale. The highest impact levers from an emissions standpoint require progressively higher levels of policy support and very large investments in individual technology development, in addition to building out enabling ecosystems. Regional differences in these critical areas are at least as striking as the similarities. Accordingly, we anticipate that regional decarbonisation pathways will not easily converge in the coming decades with differentiation persisting for a considerable time to come, given variations in the following:

- Domestic policy favourability - Regional carbon taxes, levies or allowances, or emissions trading schemes (ETS), are important mechanisms to drive decarbonisation. A number of direct and indirect signposts indicate that regional differences in these policies are likely to be persistent. Given the importance of this lever to alter private sector behaviour, this will obviously lead to regionally specific rates of higher-cost technology take-up and different rates of progress through the phases.

- Alternative low-or-lower-carbon fuels availability – This is another unique local factor. Blast furnace steelmakers in natural-gas-rich North America are already injecting the lower-emissions fuel. The Middle-East steel sector is dominated by a gas-based direct reduced iron (DRI) process. In South America, biomass (charcoal) injection will continue to be a promising abatement lever.

- The age of blast furnace (BF) fleets – Steelmaking capital stock is long-lived, which is a double-edged sword where decarbonisation is concerned. Older facilities encourage steelmakers to jump to frontier technology. A newer facility makes retrofitting or modification more attractive. The average integrated plant age in the West is approaching 50 years, and local steelmakers therefore face relatively earlier decisions for technological switching. By contrast, the BF fleet in China is only about 12 years old, while India (average age is around 18 years with more new furnaces underway) and Southeast Asia (even newer than China) have similarly young fleets. Therefore, in populous emerging Asia, transitional abatement levers such BF modification and carbon capture, utilisation and storage (CCUS) are very realistic options.

- Divergent demand for new capacity – Regional steel demand trajectories determine ‘emissions baselines’ in absolute terms. Steel emissions in most developed regions are expected to continue to decline. China will soon follow suit. However, steel demand is still growing in other developing regions. Collectively, they are expected to be the main source of growth in regional steel emissions.

- Different steel net trade positions – Steel is a globally traded commodity. While wealthy regions with marginal imports dependency are mulling ‘green border taxes’, some developing regions heavily rely on cheap steel imports to contain building costs for much needed infrastructure and housing. Meanwhile export-oriented steelmakers have to carefully balance their cost-competiveness and decarbonisation ambitions.

(Note that we do not include scrap availability and renewable power in this list, despite their great influence on regional decision making, as we class them as ‘passive levers’ embedded in the simple BAU case).

Before we dive into details of the cases we are going to discuss, it is useful to emphasise that the difference between the cases is not the amount of steel demanded: it is how that demand is met. The emissions range therefore reflects the policy and technological uncertainty inherent in any long-term simulation, but not end-use demand uncertainty. This approach is consistent with the method we apply to our integrated energy system and climate scenarios, where the same amount of final energy services are delivered in each. It is just that they become progressively more efficient in terms of primary energy and emissions intensity as they move to the green end of the policy, behaviour and technology spectrum.

In the pathway that accords with the power mix and carbon pricing assumptions embodied in the Central Energy View documented in our Climate Change report (CCR), absolute global steel emissions are likely to decline by a little less than 15% from 2019 to 2050. In this central case, the majority of steelmakers are expected to focus on process optimisation. Leading steelmakers in some regions will continue to trial and eventually adopt more costly abatement technologies, consistent with the announced objectives of a number of European producers.

In the lower carbon case, also documented in the CCR, worldwide steel emissions could fall by more than twice as much as in the Central case. A more supportive policy environment, including higher carbon prices, could foster the circular economy (higher-than-base-case scrap collection) as well as providing enhanced Scope 2 abatement opportunities for steelmakers via a swifter decarbonisation of the power mix. These conditions are likely to incentivise wider adoption of high-cost abatement levers, such as CCUS and hydrogen steelmaking. The global outcome in this case (about -30% versus BAU) hides considerable regional variation. The EU leads the technological decarbonisation effort, while emerging regions achieve a relatively smaller saving against their 2050 BAU baseline emissions. A sense of that complexity comes through in Figure 2 below. This chart also shows the bottom-up techniques we use as a basis of all our longer-term analysis.

Figure 2 Global steel emissions pathways and 2050 regional abatement by levers in lower carbon case

Source: BHP analysis; IEA.

Note: BHP Central Energy View (Central case) tracks 3◦C temperature increase above pre-industrial level. BHP Lower Carbon View tracks approximately 2.5◦C increase. IEA State Policies Scenario (STEPS) is the baseline scenario in its Iron and Steel Technology Roadmap 2020. The IEA Sustainable Development Scenario (SDS) tracks 1.5~1.65◦C temperature rise.

Our central and lower carbon cases sit comfortably between the two “book-end” scenarios from the International Energy Agency (IEA) included in Figure 2. The IEA STEPS is comparable to our BAU case in spirit. The IEA’s Sustainable Development Scenario (SDS) works towards a global temperature outcome of 1.5 to 1.65 degrees Celsius above pre-industrial levels, which requires deep and early decarbonisation across all sectors as well as a massive roll-out of negative emissions technologies. It is not directly comparable to our lower-carbon case, partly due to the fact it assumes that fewer tonnes of steel will be needed as a result of progress in ‘materials efficiency’. It also introduces a novel leap-frogging assumption for India, which we consider in the regional discussion below.

We will now examine four major steelmaking regions - China, Developed Asia-Pacific, Europe, and India - in turn.

Figure 3 Steel emissions for key regions (Mtpa CO2)

Source: BHP analysis

China (53% of global steel production in 2019, 1.8 t C02 intensity per tonne)

China is estimated to contribute more than 60% of global steel emissions today. With Chinese steel production entering its plateau phase in the next decade, and scrap availability rising strongly, passive abatement in China stands to make a major contribution to absolute emission reduction in the coming decades. We put China’s passive abatement opportunity at about two-fifths of the 2019 level: which is easily the largest absolute emissions decline among all steelmaking regions.

Even so, China could do more in steel decarbonisation: and given what we think about likely trends in lower income markets like India (see below), it will need to.

Chinese blast furnaces (BF), with their operational agility, have been taking most of the low-Fe-content iron ore available in the seaborne market. This starting point represents an optimisation opportunity to blend with higher-grade ores to cut emissions. In addition, continuous technological upgrades to meet stringent environmental standards could also drive emissions down further.